Original Link: https://www.anandtech.com/show/9805/china-calling-huaweis-media-tour-kirin-950-and-why-we-went

China Calling: Huawei’s Media Tour, Kirin 950 and Why We Went

by Ian Cutress on December 4, 2015 8:00 AM EST

Sometimes the only way to develop a relationship with a technology manufacturer beyond a simple press release exchange with a media relations team, and the odd limited-time product review sample, is to meet the people responsible for designing, managing and marketing the products. Over the past two decades (almost), AnandTech has done this with numerous companies in the East and the West to great effect, to the point where our CES and Computex schedules are effectively packed to meet up with manufacturers we work closely with to update each other on perspectives in the industry as well as progress being made internally and externally. This November, we were given the chance to visit two of Huawei’s facilities and speak to a number of important individuals at both Huawei and HiSilicon.

Huawei, A Perspective

If you’ve followed AnandTech’s smartphone coverage of late, you might recall we attended the launch of Huawei’s P8 and P8 Max handsets, with Andrei reviewing the Mate S, the P8, the Mate 7, the Honor 6 and we’ve also covered devices like the Mate 2 briefly in the past before Huawei’s push to more western-style markets and devices.

For lack of a better phrase, others have said that ‘If Xiaomi is China’s version of Apple, then Huawei is China’s version of Samsung’, and if we go by sales figures, Huawei is now regularly competing (depending on which metric you use) alongside Xiaomi, Apple and Samsung to be the biggest smartphone provider in China in terms of shipments and market share. Huawei has devices, they have the clout to mass-produce almost on demand, but they are having issues expanding outside of their main consumer base, which is part of the reason why these media tours are taking place. Having read through the trips of several previous journalists, it was slightly amusing to hear that a common factor brought up in discussions is that the name Huawei seems to be difficult for westerners to pronounce if they’ve never heard it before (for clarification, try hwa-way or hugh-er-way). Interestingly, Huawei doesn’t see that as much of a barrier. I could certainly imagine members of my family seeing the name ‘Huawei’ and not having an idea how to pronounce it.

Nevertheless, Huawei’s circumstances in the global market has been one reason why we have wanted to get into deeper contact, especially as one of Huawei’s key technology assets is its custom silicon design capability for its SoCs. From their subsidiary company HiSilicon, whose roots can be traced back to the 90's, they produce chipsets designated ‘Kirin’, which implement ARM microarchitecture designs with other IP elements to form their own SoC, rather than relying on third-party designs such as from Mediatek, Qualcomm or Samsung. As part of our tour, we were present at the official media briefing (translated real-time from Chinese) for HiSilicon’s latest chipset, the Kirin 950. As mentioned in our announcement piece, this chipset is built on TSMC’s 16nm FinFET+ process and features quad A72 and quad A53 ARM processors as well as a new custom image signaling processor, Cat 6 LTE modem and dual memory controller support.

On the subject of SoC design, from the outside at least, if we were to consider Mediatek and Samsung both ‘Tier-1’ implementers of ARM’s microarchitecture designs, as opposed to Apple and Qualcomm who take the ISA and do their own µarch designs, then from the outside HiSilicon's Kirin lineup seems to be eying the former development. I prefixed that last sentence with ‘from the outside’ because that distinction is important – HiSilicon has been closed to any in-depth discussion of the design, and the devices we have tested so far do not necessarily produce anything new into the ecosystem. Either we are missing a trick in understanding the design from the top-down, or not understanding the design philosophy behind why Kirin exists as opposed to an off-the-shelf Mediatek or Qualcomm comparison. As further explained in part of our media tour, we spoke to a number of individuals at HiSilicon for the purpose of understanding their perspective, and hopefully educating ourselves and passing this information on to our readers.

The Purpose Of This Piece

To augment the more professional analysis we usually do at AnandTech, this piece is more of an overview of the Huawei media tour combined with a look into corporate strategy, how Huawei sees itself, and where the difficulties might lie in their goals. This piece is written in a more colloquial style than some of our other write-ups, but even if everything on this trip we saw was cherry picked (see the next page), there is still some value in breaking down a metaphorical company ‘black box’ where we have products coming out on one side and press releases/marketing on the other with some magic in-between. In the past we’ve done this with HQ visits to ASUS, ECS, MSI, Logitech and others, as well as a long series of interviews with Intel and ARM. The fact that this is a company based in China that isn’t called Foxconn suggests that even if all we see is ‘just another smartphone factory’(™), we can at least probe the corporate structure and find out what makes a company like Huawei tick, asking questions and generating a long-term dialogue between us.

Huawei’s main building, Shenzhen site

Huawei's Media Tour, and Why We Went

When it comes to companies based in China, the obvious tropes of secrecy come into play. Most companies want some level of secrecy, but some have abstracted themselves through PR firms to avoid direct media contact. Despite these companies being big behemoths in their own market, with a back-thought to large towns of 10,000+ people devoted to one factory, access from our side of the fence can be limited. In order to get that access, and to meet face to face, typically requires an invite to their facilities purely on their terms: they fly you out and they dictate what you see during that trip.

For those journalists in the industry reading this, some of you may have come across recent critiques from both inside the tech press and from readers about these trips, as a form of payola to generate content that flatters the company and whether this is an ethical process at all, as the journalist or editor is accepting a ‘free trip’ which could cloud their future judgement. There have been many situations when a ‘free trip’ becomes a series of posts or ‘look at what we did’ videos, without any critical analysis or development to the industry (or any clarification of who paid for which product placement, which can be deceptive at best).

But with the right attitude, depending on the journalists or editors you follow and trust, one can retain the element of editorial independence when getting involved in this. As mentioned already, the crucial part of accepting these trip offers is to talk to and understand the people that matter most, in a process to open doors for the future, and for some of these companies, taking that media tour when offered is that process. If you don’t take that step, then the relationship stagnates, and as a journalist you end up pumping out more of the same, rather than trying to be the best you can be and generate the sort of traffic that makes who you write for unique.

This sounds like a boring setup to an opinion piece on ethics in technology journalism, but I promise it is not. But these are the foundations on which AnandTech accepts any ‘paid for’ trip, along with maintaining editorial independence but focusing on the relationship, and circumstances evolved recently such that one of the companies we’ve wanted to probe in more detail for a while gave us that opportunity this November. In 2015, Huawei, through their PR companies and contractors, has been giving short media tours of its technology facilities to small groups of journalists this year, as well as group interviews with important VPs up and down the chain. Note that at the top of the piece I mentioned that these trips are dictated by the company involved, so we were under no disillusion of the circumstances which would be presented (I can’t fault someone from doing their job in all honesty), but Andrei and I made our way to both Shenzhen and Beijing as part of the media tour. Needless to say, we requested meetings with the technical teams right away.

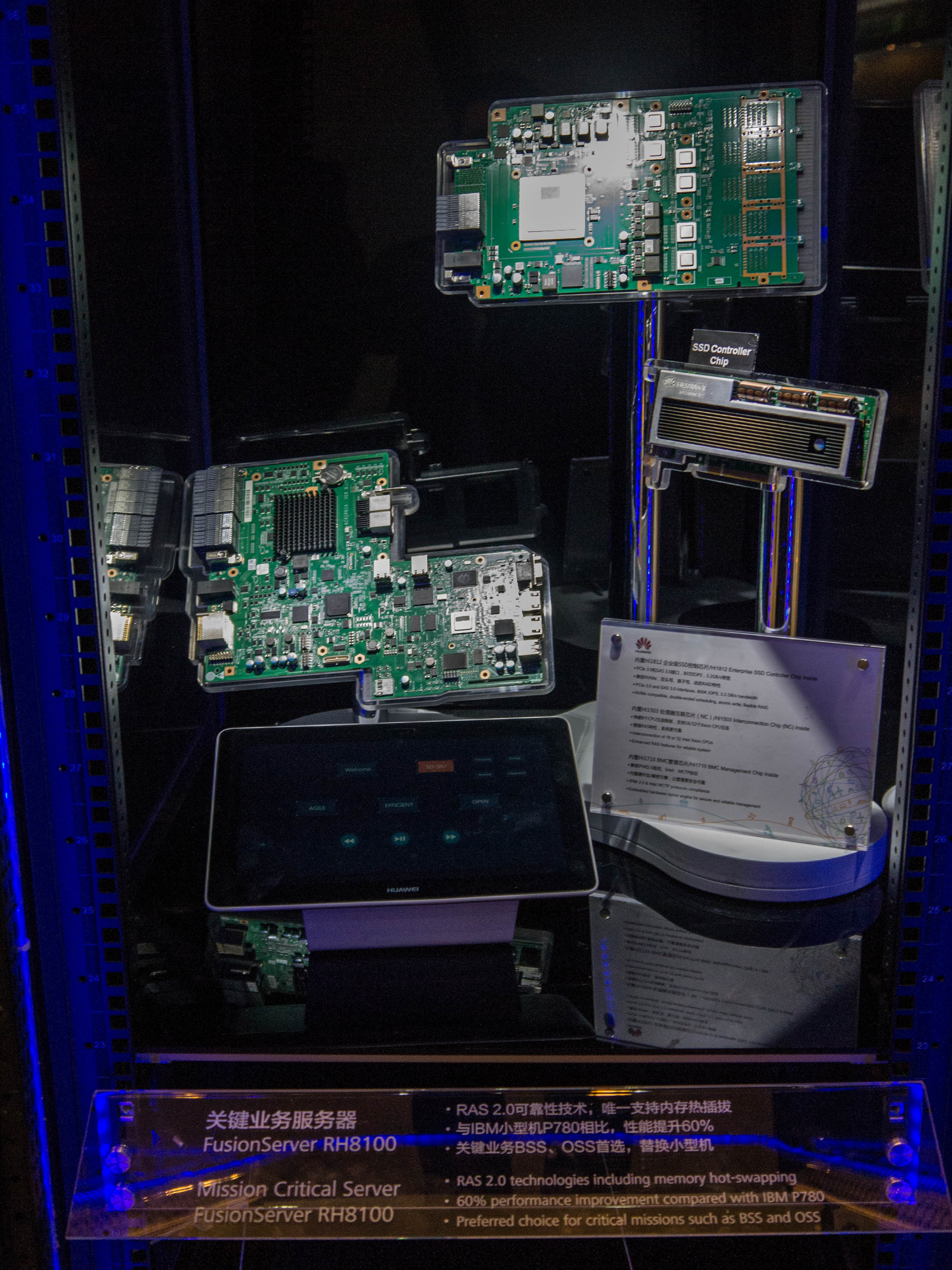

Examples of HiSilicon/Huawei's Custom Silicon

The Tour

From first contact, the travel arrangements for the tour changed multiple times, from visiting factories and research facilities in Shenzhen/Dongguan followed by R&D tours in Shanghai, to a day with six or seven VPs for 1-on-1 discussions, to a new Kirin family release in Beijing. In the end, the tour started in Shenzhen at a very typical set of smartphone testing labs in nearby Dongguan, followed by a flight to Beijing for the Kirin release and further interviews and discussions. During this time, we spoke in depth with Mengran Duan, the president of Huawei’s watch products, a tour of Huawei’s device testing labs, discussions with Bruce Lee, VP of the Handset Product Line, and the announcement of the Kirin 950. Beyond this there were discussions that we cannot talk about at this time, but for the benefit of our readers they were certainly fruitful and should offer us more perspective (and routes for information) in future Huawei-related discussions.

The US Media Tour group – spot your favorite editors

To add an element of amusement in the mix, as with any Trade Show such as CES and Computex, a lot of companies are free-flowing with goodie bags. Most of it is normally junk that’s thrown away almost immediately (I have a dozen mousepads I don’t need, and even more USB sticks of ex-product kits). All of it is designed to curry the favor of the journalist and to butter them up with freebies (so keep an eye on the journalists you trust), but sometimes there’s a high quality notepad or something worth keeping or passing on. Similar to Huawei’s previous media trips earlier this year, they sampled the tour participants with their latest US-based handset (which we’ll review) as well as a small wearable extra - the handset was augmented with the Talkband B2 wearable and the above framed memento of the group of media during the trip. We also asked about how Huawei will be sourcing the first Kirin 950 devices on the market, namely the Mate 8, and were told to keep our email clients open for details when the time comes around.

It’s Just Another Smartphone Factory™

In a very typical stereotype, the campus in Shenzhen for Huawei has around 30,000 employees over 2.5 square kilometers, with some of them located in housing nearby within the local area. Perhaps quite interesting is that there are Foxconn offices across road, to the extent that at one T-junction there was a sign for left saying ‘Foxconn’ and a sign for the right saying ‘Huawei’. It has been noted that Foxconn has manufactured products for Huawei before, and thus I can imagine being so close to each other has its own benefits.

Make sure you make the right turn

Needless to say, a campus this size is very difficult to ‘tour’ around, especially as we had special presentations and meetings with the President of Huawei’s watch division discussing the Huawei Watch, lunch with the Director of Global Relations as well as a tour of the testing facilities during the short time there.

The standard rules apply for a company of this nature – there are tall corporate buildings with product areas and descriptive walkthroughs of what the company does, with professional meeting rooms that have in-house catering, whereas the technical offices and data center management are generic looking concrete places that are mostly no-go areas for media visits. This dichotomy between ‘on-show corporate’ and ‘the general workforce’ is mirrored in companies around the world, to the extent that we also had lunch in a special canteen for guests with a background band as you entered.

Musical accompaniment in the executive dining hall reception

During lunch we ate and talked with the Director for Public Relations, rather than eating in the casual employee canteen and experiencing the potential mêlée that comes with that. However, the campus is designed with an element of beauty in mind, under the premise that the CEO has a degree in architecture, and wanted the campus to reflect an element of style rather than be another box hidden in a corporate mountain. It was at this point that it was suggested by Andrei that the ultimate tech press clickbait article would be ‘An In-Depth Look at Huawei’s Architecture’ and it being about the buildings and landscapes of the campus, rather than insights into the company's silicon or devices.

Part of the tour was also to one of the smartphone testing laboratories, although we were not allowed to take images inside of the facilities. If any of our readers have seen our articles in the past about this (such as ASUS), the usual array of drop tests, twisting tests, insertion, vibration, high temperature, low temperature, humidity cycles and battery presses were also present on site, although RF testing is performed on a different campus than the one we visited. So when this page started with ‘It’s Just Another Smartphone Factory’, the reality is that almost all of them are like this, as they all need to perform similar tests dictated international and industry standards. The key here is individualization - most of the key elements to what a company does with their product is in the hardware design stage or software, rather than product testing, unless water/dust resistance is a key factor, or additional MIL-SPEC (military standard) is needed. Even then, for MIL-SPEC, one would assume that the testing would be outsourced if it only applied to a few devices, rather than purchasing all the equipment.

It’s Just Another Smartphone Manufacturer™

However, part of the tour of the main Shenzhen campus stood out to me (Ian) personally. Whenever we speak about Huawei, the focus is always on the smartphone market, because that is what most people can relate to as that is what our readers can actually hold something made by Huawei in their hand. But interestingly enough, consumer smartphones only account for 30% of the company’s revenue. Huawei puts a lot of resources into backbone networking and infrastructure, which accounts for 40% of the revenue.

A Huawei Cloud Base Station with many network ports and custom silicon inside

Arguably, if we were trying to cover the important markets for some of these companies (such as MediaTek as well), then networking and infrastructure would be as important as smartphones, if not more so. So we were told about Huawei’s march to 4G/4.5G/5G, as well as MIMO antennas, base stations, but also data analytics management and services to mobile carriers and other markets.

One element remained consistent within this: Huawei hardware was in the machines that powered them, which included a large array of HiSilicon ICs and heatsinks covering almost everything. There were quite clearly a number of devices attached to lots of Nanya memory (up to eight dies on one example board shown), as well as a series of what looked like HiSilicon PCIe-like switches.

HiSilicon was founded in 2004 as a subsidiary of Huawei, but the company has roots further back into the 90's when it was still known as Huawei's ASIC Design Center. Ever since, the subsidiary has diversified in a lot of market segments such as mobile, networking, video surveillance, DVB or IPTV. The company was proud to proclaim that it was the first to offer silicon based on ARM's Cortex A57 - these are server SoCs with up to 16 or 32 cores and 32MB of L3 cache. The DVB and TV market is also one of the rarely talked about markets in which companies such as MediaTek and Samsung offer a wide range of custom solutions, and it seems HiSilicon also has a range of products for the segment such as an A17-based SoC that we hadn't heard of earlier.

Custom Huawei SoC, relating to networking

In many of the devices on display in Huawei's showroom, there was a number of copper and fiber connections in almost everything, to the point where even the mini small-cell implementations had 10GBase-T and seemed to be powered by PoE (power over Ethernet).

We asked about Huawei’s application in this space, and the answer was from origin to end user – from the data center to device. Within this, the data analytics part was interesting. Carriers that use Huawei backbone implementations, either by direct purchase or lease, have access to their monitoring software and can analyze what sorts of data their users are processing – either pure data, certain web servers, streaming video and so on. Huawei stressed the point that while they can provide general hardware or work with specific customers on a custom solution, the actual processing of what their customers want to do with the data their clients produce is up to them.

“4-in-One Multi System on Chip Smooth Evolve to LTE-A”

capable of GSM, UMTS, FDD LTE and TDD LTE

With the internal metrics of throughput or the results of the customer analyzed data, both the customer and/or Huawei can deploy infrastructure to cover blackspots or enhance the direction of content – in one scenario, we saw a mockup of Huawei’s software which had what can be described as ‘Amazon Recommendations’. It was almost as clear as ‘your users seem to be requiring this (a) in regions (b)(c), we recommend the following products (x)(y)(z)’. There was no particular mention of any common PCIe accelerators usually associated with data analytics (Xeon Phi, GPUs, FPGAs), which makes us wonder how much is custom HiSilicon compared to off-the-shelf parts. Of course within all this, Huawei offers a sustained servicing and maintenance package, similar to how big tech firms bring in the revenue after selling the hardware.

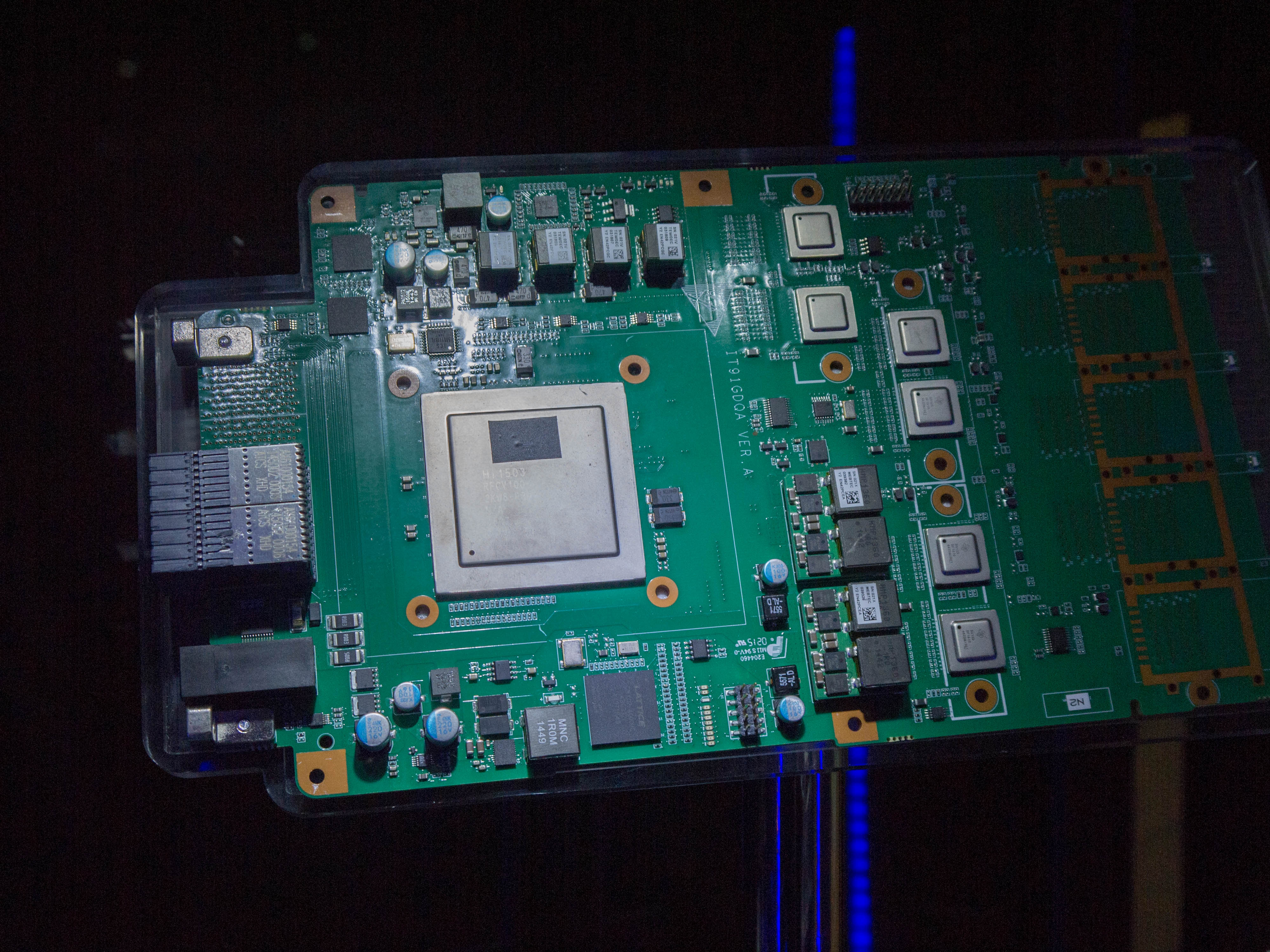

So here’s in interesting thought – Huawei is in the SSD business. That pretty much came out of left field, but it in retrospect it should have been one of those things that was probably pretty obvious. Here’s a PCIe SSD, with a custom HiSilicon Hi1812 controller supporting PCIe 3.0, NVMe, 800K IOPS and 3.1 GB/s of read bandwidth with MLC planar NAND. That makes it sound like there’s a RAID controller in there, as no individual single controller we know of can reach those speeds (Samsung’s MGX can do 2.5 GB/s). There’s no telling if it uses an ARM IP variant or a custom ISA developed by HiSilicon, which makes it interesting. Underneath the explanation of the Hi1812 are a couple of other choice parts, scratching the surface of just how deep the rabbit-hole goes.

Because Huawei has HiSilicon to develop custom hardware and SoCs fit for purpose, it allows the vertical integration element to be rather interesting from the outside. We’ve talked before about how HiSilicon keeps its cards close to its chest, and in a similar situation to some of ARMs partners that do not make announcements, we can start to get a picture of just how deep HiSilicon permeates into Huawei’s infrastructure division and how most of us probably have data that has passed through Huawei-based networking products through the web, and how much the hardware is a part of that process.

Blade-like modular baseband-station and antennas

For any of our UK readers, with the recent trip of Xi Jinping to the UK you may have heard the recent discussions in the UK about having China invest in our new power plants. The concept of this for some citizens results in the fear about having China as part of that process. But most people don’t realize that China as a provider is already in the ecosystem – when people access the internet, their data most likely goes through a series of hops that might include Huawei network switches between device and <insert email client> or <insert social media network platform> or when a website script may call on services elsewhere on the web and you don’t even realize. So aside from the commonly named network infrastructure players in the west, such as the commonly known Cisco, Alcatel-Lucent, Nokia or Ericsson, there are players such as a Huawei or a MediaTek that have their arms in the game as well. Given how vast the market is, especially for total worldwide revenue, there are many players that the general public (or even technology magazine readers) won’t have ever heard of.

Moving The Smartphone Target Market

It may seem obvious but part of point of trips is to generate dialogue. Huawei is interested in what we have to say about the perception users outside China have of them, as well as our opinion on their latest product trends, and we’re interested in Huawei both internally for how they work, generating ideas/products, but also externally and how they approach different markets, especially moving into North Americas and expanding in Europe.

While Huawei has been on the periphery of most tech media since the launch of the P1 and the P2, and more prominently so with the Mate 7 and the P8, they are still a brand with little recognition outside of technology enthusiasts in the West. Huawei is well known in China, and product launches are well attended with lots of interest, as well as deep discussions with the media, but it is only recently that they have begun to extend invitations to similar outlets in the west. Part of it is to explain their story, their philosophy, and the other part is to explain to journalists such that they can run their own interpretation, providing Huawei smartphone reviews with at least an element of analysis about the company in general at the same time.

A cynic might argue that in order to get a foothold into the US or expand in EMEA, there needs to be a combination of a large targeted marketing campaign as well as a definitive product individualization, such as an Apple device, or a Samsung, though to LG’s Flex or HTC’s characteristic look. But even then, HTC’s current situation is in a state of flux despite heavy marketing for a number of reasons, meaning that a big push has both potential risk and reward. As part of this trip, we discussed with Huawei on how exactly we perceive the smartphone market, what are the interesting elements of it and how Huawei can open up to us with both information, structure, and sampling.

It was quite telling that during a roundtable discussion, the journalists around the room were asked what sort of products they were interested in. It was almost a unanimous chorus pointing towards the flagship models for two main reasons – firstly, most other companies provide flagship devices, so there is a rolling comparison and knowledge of an adapting market, but the second point was that the flagship devices typically bring in more variance, engineering prowess and showcase the best of the company talent. Both points are certainly true, and I (Ian) personally can’t disagree with their responses.

The Huawei Mate S - the company's current flagship device

My argument was slightly different, especially if we compare to the industries I regularly write about; from my perspective, I’d prefer to test the popular devices. With a $600 smartphone, everyone has an opinion on the design, the hardware, the benchmark results, or simply fanboyism, but not everyone has $600 to spend. While a lot of users might discuss the virtues online, or debate over small details, the reality is that a good portion will opt for something around the $250-$300 range for their main device or family devices, depending on contract, region, availability and other features. This is similar to when we get $2000 laptops, or $500 motherboards – lots of discussion, but in reality fewer people will buy them and go for the $800 2-in-1s or sub-$160 motherboards.

Andrei brought up a good point regarding this, which relates back to the first point about mainly reviewing flagships – if you test in the $250 range for smartphones, then there are 80 or so devices to choose from and the review either has to be in a vacuum comparing to almost nothing or based on the limited knowledge of what exactly is in the market, as it's impossible to review every alternative that exists out there. It provides an interesting dilemma for companies like Huawei and their competitors, because depending on what the media wants to look at will dictate what products the manufacturers will sample for review and/or how many are distributed. Thankfully Huawei are open on this and are willing to entertain our future device requests.

This becomes all important for entry into their non-standard regions, if they feel that there needs to be more presence that just a flagship model. Huawei over the years has slowly reduced their smartphone lineup from around 80 new models a year to fewer than 25, even though most of us only ever discussed three or four of those in 2014/2015 (P8/P8 Lite, Mate 7 and Honor 6). Chances are that the metric of devices moving into the west should increase over time, in both flagship and mid-range markets especially.

Discussing Corporate Structure, Strategy and Kirin 950

As noted in the last few pages, Huawei’s structure falls into multiple domains. As a result, the three main groups involved in research, design and product are the Consumer Business Group (Smartphones, Mobile Broadband), the Carrier Business Group (Core Networks, Wireless Networks) and the Enterprise Business Group (Infrastructure, Data Centers, Security). In discussing the handset division with Bruce Lee, VP of the Handset Line Division, we learned that Huawei invests 10% of its revenue for the CBG back into research and development, with around $20 billion revenue expected to 2015 resulting in $2 billion for R&D.

To put this into perspective for other fabless semiconductor businesses, MediaTek at their recent Analyst day quoted around 20-30% of the revenue for R&D (~ca $900-1200m). It was not indicated if the 10% value given to us was is a function of HiSilicon's investment, or if this was CBG, or Huawei as a whole - the Mediatek number as also broad and encompasses the company compared to the number from Huawei which is most likely just one division of the company. This makes investment spending difficult to compare, given the different markets each of the two participate.

It was clear that Huawei is very conscious about their brand image, and on this media tour it was reiterated that both the pronunciation of Huawei and the perceived opinion purely of being from China might weigh heavily on that direct image. We were told that despite this, due to Huawei’s long tenure as a global brand, they saw merit in pursuing (at least in the handset market) the brand recognition that comes with tying their enterprises together. Constant year-on-year talks internally on potential branding issues are being held, but despite any perceived conflict of utility or nationality ‘Huawei’ as a noun to associate with mobile devices is here to stay for brand combination. To that extent, Huawei was happy to promote their places in Forbes' lists and the Brandz ‘Top 100 Most Valuable Brands’ list at #70, valued at $15.35 billion.

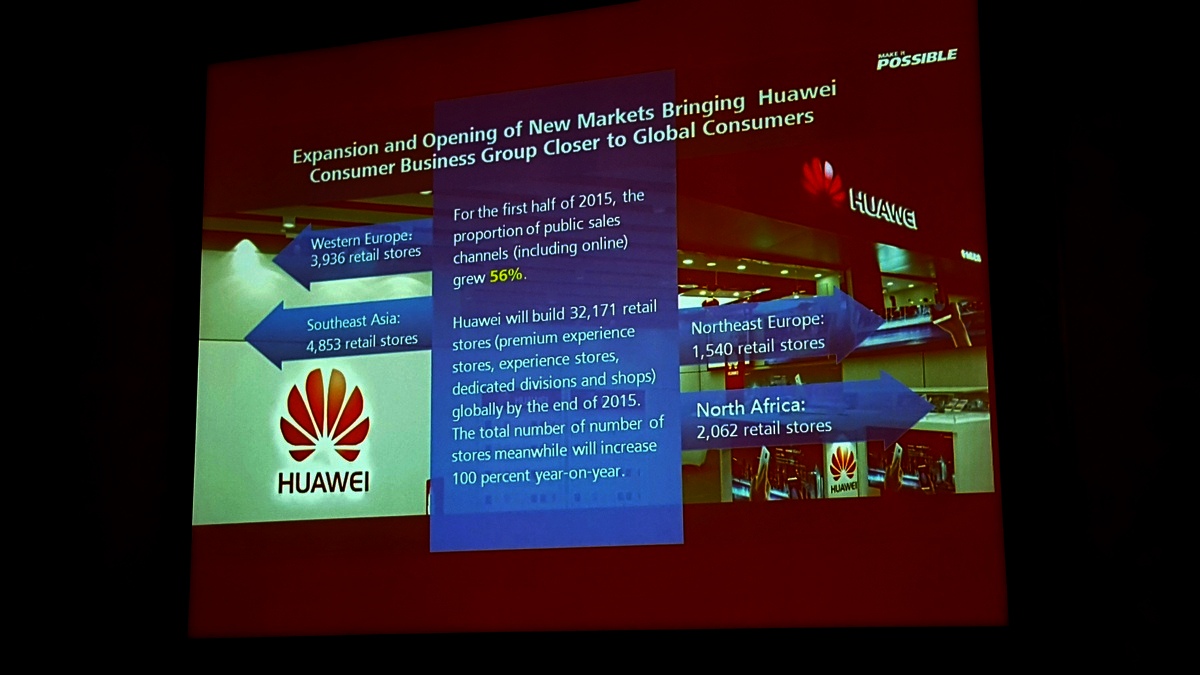

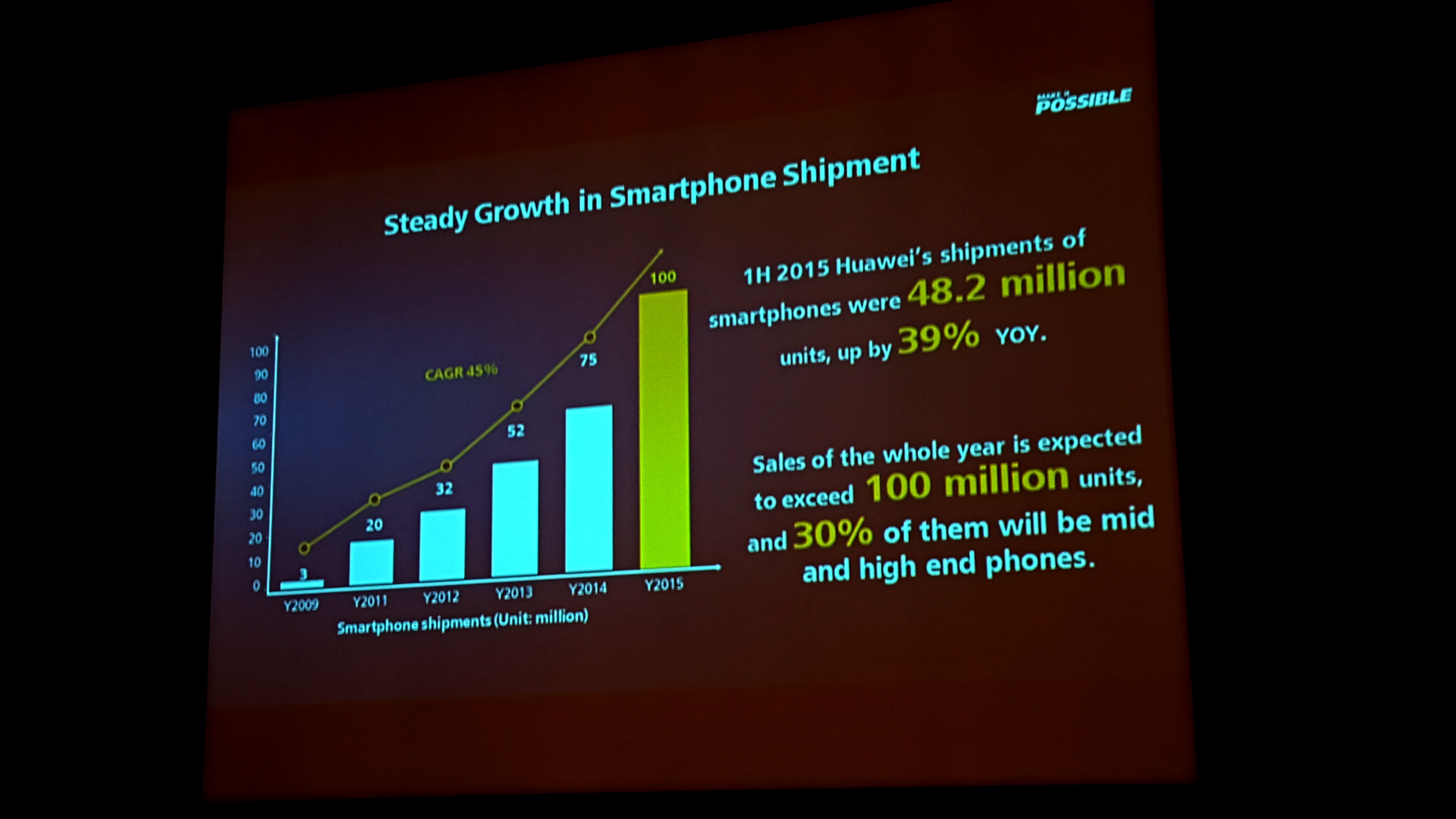

Part of that mantra is a large push from Huawei for their presence in stores globally, either as segments in a general smartphone store or their own branded premises. As a result, as shown on the slide above, the number of sales channels for Huawei in 1H2015 has grown 56% with a total of ~32000 new sales outlets being built in 2015 alone. This is a heavy contributor to the sales figures in smartphones, which for 1H2015 is around 48.2 million (+39% year-on-year), with end-year figures projected at 100 million. Huawei was keen to stress that 30% of these sales (so 30 million units) were mid-to-high end smartphones, which Huawei classifies as any handset over 400 Euros. In that regard, 30 million units at 400 euros gives 12 billion euros in revenue, at a minimum, on just 30% of sales. This according to Huawei leads to a CAGR of 45% since 2009, when they sold only 3 million units in a year.

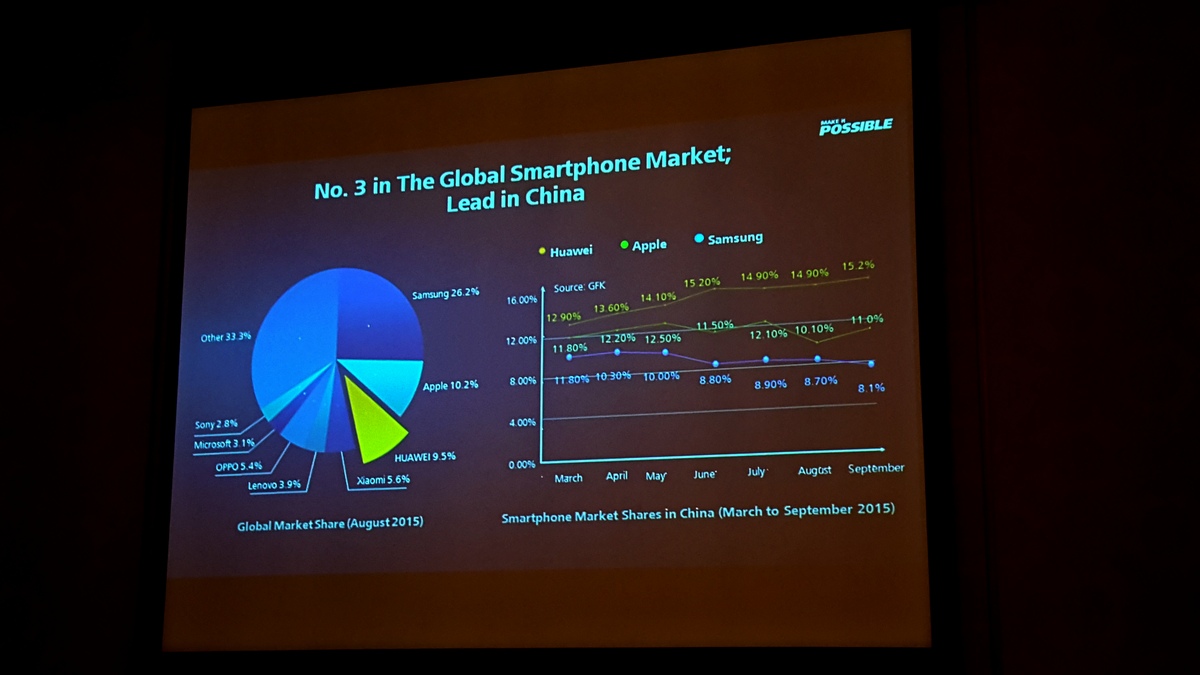

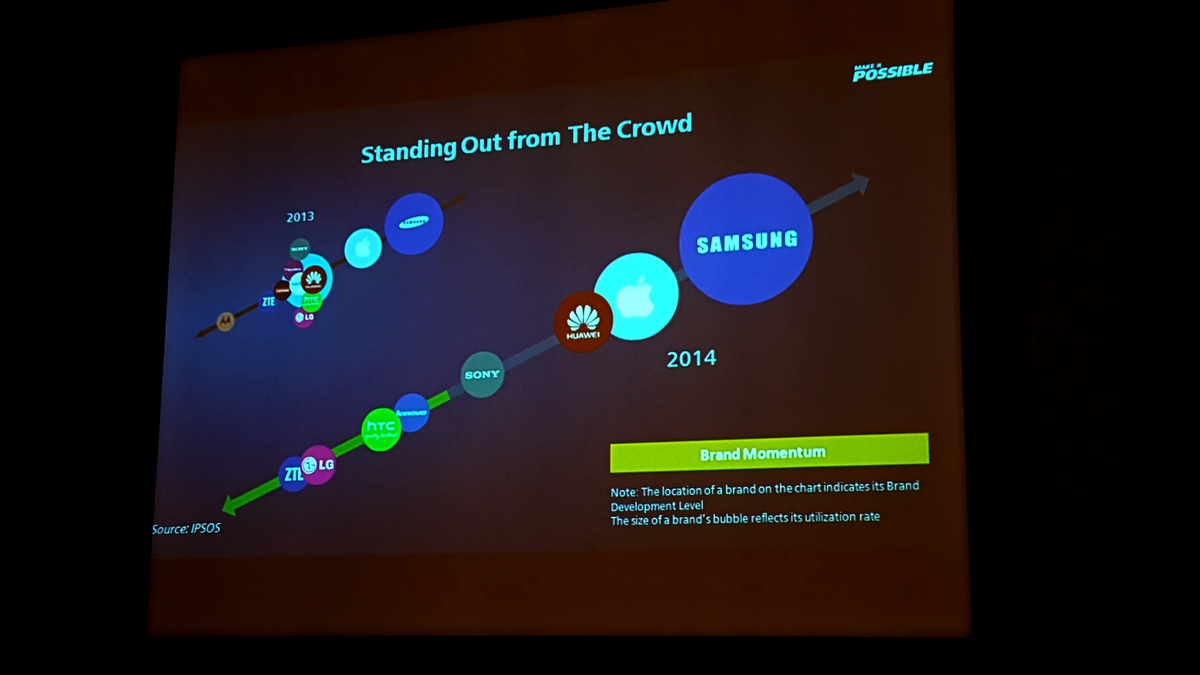

Huawei was keen to talk market share, which led to the chart using GfK data. They have put Huawei in at #1 for China with 15% of the market share, absorbing Samsung’s market while Apple hovers around 11-12%, and Huawei at 9.5% globally. The other home grown provider, Xiaomi, sits at 5.6%. We asked specifically about Huawei’s thoughts on Xiaomi as an important rival, but the interesting answer came back in that while Huawei sees Xiaomi as a significant player in the Asian markets, but at this current time on the global scale they only look towards Apple and Samsung as the major players.

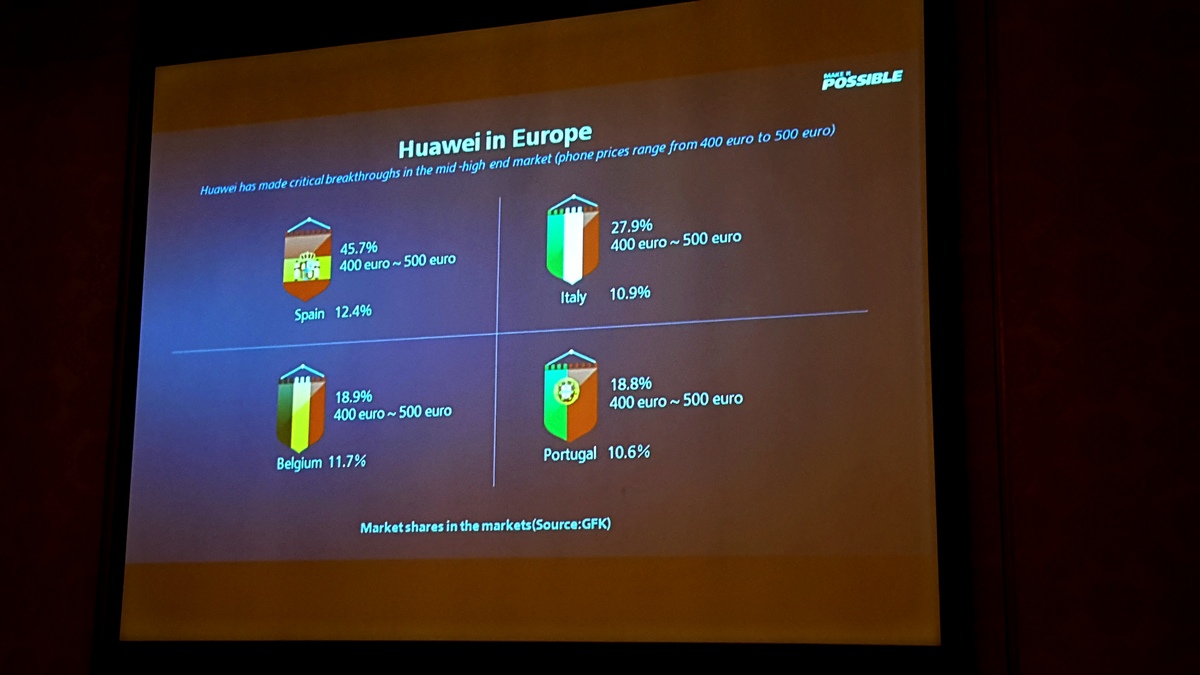

Because of the high-to-mid smartphone sales numbers, we were given a small glimpse into how Huawei is approaching some of the specific regional markets in Europe, with penetration figures. Now ultimately these figures are very cherry picked, but they show that out of the €400-€500 markets:

- In Spain, Huawei has 12.4% (€400-€500 is 45.7% of total)

- In Italy, Huawei has 10.9% (€400-€500 is 27.9% of total)

- In Belgium, Huawei has 11.7% (€400-€500 is 18.9% of total)

- In Portugal, Huawei has 10.6% (€400-€500 is 18.8% of total)

It’s worth noting that for those Spain numbers, 12.4% of that one market, of which the market is 45.7% of the whole, means that Huawei’s mid-to-high offerings account for 5.67% of the whole market for Spain. The reason why Huawei is quoting numbers like this is to show their presence in that high-end smartphone space where typical middle-class users with a bit of spare spending money are deciding to buy their devices.

For high end devices, we were told that the Mate 7 has sold over seven million units, the P7 has sold over eight million units, and the P8 that was released back in April is already at three million units. We probed further and learned that the sales curves for the P8 are currently outclassing the P7 for the first few months after launch, but exact graphical representations were not on hand at the time. We asked for them, and our hosts promised to at least put in the request if these numbers can/will be made public.

Throughout all of this, it became clear that there was a elephant in the room. Because this media tour was for publications that have HQs were in the US, a lot of discussion around Huawei’s presence in the United States was on the cards – or more specifically, the lack of Huawei’s presence. While there has been a number of handsets that have made it none of them are Kirin powered but instead use Qualcomm platforms. Of course, a Kirin device could be sourced online, but Huawei has not yet put Kirin in the hands of the general public and initiated a big push beyond handing devices to smartphone reviews and launch events.

Historically we know this to be an issue surrounding the unique CDMA requirements for the US market, and we were informed that Huawei’s approach is multilayered. At the top is their collaboration with Qualcomm’s SoCs which they feel fit in very nicely with the current North American desire and distribution – for the tech press it’s a known quantity, a known company, and there can be straightforward comparisons between other handsets allowing Huawei’s design philosophy to show through. The next layer surrounds having the right IP to enable CDMA, let alone have it certified on a Kirin chipset. Huawei said that while the 950 is currently not part of this program, and they are working on licensing the relevant technologies (from Qualcomm) in order to do so, which may or may not be in future roadmaps but there are plenty of variables to this equation and it is not as straightforward as one might imagine. The third is time, as CDMA certification on a new chipset (regardless of the licensed IP) is both expensive and long, and Huawei needs to decide if it is the right thing to do within their strategy.

At this time it presents a difficult situation for Huawei – the desire to be as vertically integrated as possible and yet still penetrate one of the largest markets in the world, despite the fact that there are no guarantees of success. It was remarked on several occasions that firms based in China such as Huawei are often seen as conservative and won’t rush certain aspects of their design without a guaranteed payoff, although that attitude is changing somewhat with Huawei given their push with TSMC’s 16nm FinFET+ node on the Kirin 950 chipset, and being the first to build a fully integrated mobile SoC on this process. Along with custom IP efforts such as a hybrid LPDDR3/LPDDR4 memory controller, Huawei’s was able to build up a new Imaging R&D division allowing it to build a custom image signal processor, offering another point of differentiation and potential.

Huawei currently sees itself on the up, there is no doubt about that, and their willingness to open up further to journalists outside of China is a very pleasing step. For the smartphone market, Huawei sees itself in a quite comfortable third position worldwide, sitting behind the big two and constantly growing. There are barriers to overcome, both with design implementations and local market applications.

Final Thoughts

All truth be told, when an electronics manufacturer opens up we stand to gain a great deal of insight into how they think and how strategies formulate. Sure, it’s a question of speaking directly to the people that actually make the decisions, otherwise questions and answers never go through the chain. But also as an editor, from my perspective, it is important to understand when you are presented with a standard PR answer and ask the right questions sufficiently in order to get to the heart of what makes a company tick. There will always be things that a company will never tell you, either due to liability or the level of trust they have with you, or there might be some discussions that remain strictly behind closed doors.

As we tell every company we meet, those closed room discussions, despite not directly producing content for us as technical media or analysts, are just as valuable as on-record meetings and can actually be really helpful in understanding perspective or technical details. Even if we do not write about what is said, it enables another layer of conscious or sub-conscious consideration and analysis about the industry for when we write about other topics, helping us translate what we see into the wider picture. Understanding why from a bottom-up perspective is just as important as the top-down, even more-so when looking at trends and directions and being able to educate users and engineers alike.

In that regard, this trip has established a new level of dialogue between Huawei and AnandTech in order for both sides to understand each other more, from our understanding of the markets and devices to their diverse silicon and product portfolio. That rapport and direct line of communication to those who turn the cogs which we did not have before is important, with respect to handsets, silicon, and wider corporate strategy. It is clear that Huawei wants to expand into more markets beyond their standard Chinese base, and has dipped its toe into leading the market with TSMC’s 16nm FinFET+ node in the Kirin 950. The phrase ‘premium brand’ was a common theme throughout our trip, and the numbers back that up. Moving from 3 million handsets in 2009 to 48.6 million in the first six months of 2015 alone means that the investors are all happy, especially given that 30% of those are high-to-mid level devices at a cost of €400 and up. Being partially vertically integrated through its HiSilicon subsidiary allows it to reduce cost, spend on R&D and provide a custom product as long as it is well executed. While this is going on, Huawei’s two other business groups on services and infrastructure account for the other 60% of the company, which are also both benefiting from the HiSilicon synergy.

Huawei does still have several mountains to climb however, this much is obvious. When speaking purely about the handset business, when striving for that premium brand status, its presence in North America is still a way behind the two major players. This stems from several factors including a CDMA licensing and certification issue preventing Kirin chipsets in North American models, but also an issue regarding the perception of some users that will not want to hand over money for a device made by a Chinese-based data company, especially if they cannot pronounce the name. Arguably the first of those issues is easier to crack about CDMA, such that one solution to Kirin might be to produce a die without an integrated modem, similar to Apple, but both of the issues above will have severe implications on Huawei’s ability to expand in the US. The Huawei watch too, as a dip into the wearable space, comes with many variables on style, size, applicability, usefulness, ecosystem, and others – sometimes a single model can be deceptive when users have more unique tastes and perhaps want something more/less than a classic watch design.

For the rest of the world where CDMA isn’t a factor, the latest Kirin 950 chipset needs to be a proven entity and tackle the big players in Apple’s A9, Qualcomm’s upcoming Snapdragon 820, Samsung’s Exynos 8890 as well as other upcoming custom designs. Samsung is the only member in that list with their own fabs, meaning the others will have to pay top dollar for a lead in semiconductor manufacturing. Beyond that the quality of the designs for performance, power efficiency, custom IP blocks and software integration will also be up against back-end production of the silicon itself. It comes across as a fairly daunting task for one of these manufacturers to get all the pieces in place for a new flagship handset every year that builds on the last. In order to be successful they have to execute well in every area every year, to which we’ve already seen some failures and successes.

Both Andrei and I were quietly surprised with the Kirin 950 announcement, and felt positive for the 950 as it offers some interesting innovations (first smartphone A72 cores, first hybrid memory controller, new custom image signal processor, low power i5 sensor hub with compute capabilities in an ARM Cortex M7). It will be interesting to see how much we can decipher about the new chip compared to the old, especially when we have new cores (A53/A57 to A72), a new process node (28nm to 16FF+) , new custom IP and so on. When we get a device into test, teardown and produce numbers, they will tell the story. But as is obvious from our trip that smartphones are just the tip of the iceberg for Huawei.