Original Link: https://www.anandtech.com/show/8602/the-state-of-sandisk

The State of SanDisk

by Kristian Vättö on December 5, 2014 8:00 AM EST

Back at Flash Memory Summit I had the opportunity to meet with all the key people at SanDisk. There is a lot going on at SanDisk at the moment with the Fusion-io acquisition, TLC NAND, and other things, so I figured I would write a piece that outlines SanDisk's current situation and what they're planning for the future.

I'll start with the client side. For SanDisk the big topic at this year's Flash Memory Summit was TLC NAND and we were given a sneak peek of the SanDisk Ultra II back at the show, which was then released a few weeks later. Since we have already reviewed the Ultra II, I'm not going to talk about the drive itself and its technical merits, but there are a few things that Kevin Conley, senior vice president and general manager for SanDisk's client business brought up about TLC and the client market in general.

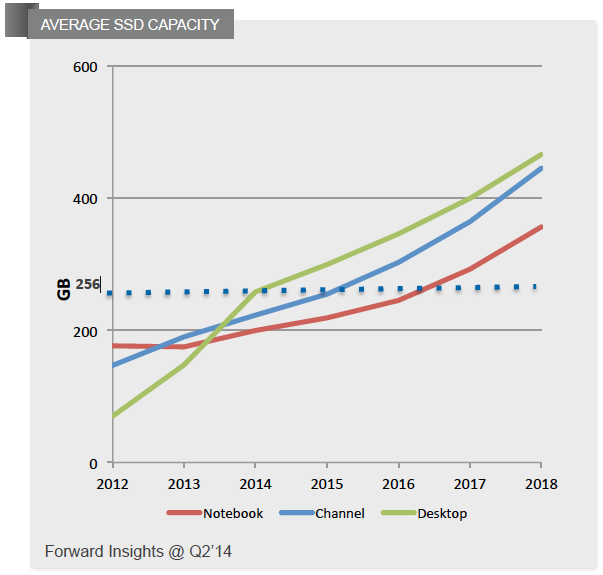

I'm sure most of our long-time readers remember how SSD prices plummeted between 2010 and 2012. The reason for that wasn't a breakthrough in NAND technology, but merely the fact that all manufacturers increased their manufacturing capacity with the expectation of exponential NAND demand growth. As you can see in the graph above, the industry bit growth was over 60% year-over-year between 2010 and 2012, which lead to oversupply in the market and deflated the prices.

The reason why all NAND manufacturers invested so heavily on capacity increases was the popularity of smartphones and tablets; it was expected that the average storage capacity would increase over time. Basically, the NAND manufacturers assumed that decreases in NAND prices due to smaller lithographies would translate to higher capacity smartphones and tablets, but in fact the mobile companies chose to save on onboard storage and invest in other components instead (camera, SoC, etc.).

It's only been recently that smartphone and tablet manufacturers have started to increase the internal NAND and offer higher capacity models (e.g. the 128GB iPhone 6/6+), but even today the majority of devices are shipping with 16GB, which is the same capacity that the low-end iPhone 3GS had when it was introduced in 2009. Of course a large reason for the reduced sales of higher capacity smartphones/tablets has a lot to do with pricing, where 32GB devices often cost $100 more than the 16GB model.

Since the NAND manufacturers are now adding fab space at a slower pace, they are looking for alternate ways to increase bit growth and scale costs down – and that's where TLC kicks in. Because TLC packs in 50% more bits than MLC (three bits per cell instead of two), increasing the share of TLC production is an efficient way to boost bit growth without additional fab investments.

Currently about 45-50% of SanDisk's NAND production is TLC and by next year TLC will be overtaking MLC in terms of production volume. Note that SanDisk will have 3D NAND ready in 2016, so the graph doesn't imply that SanDisk will move to TLC-only production in 2017 – it is just the 2D NAND production moving to TLC since it will mostly be used in applications like USB flash drives and other low cost devices, while 3D NAND will be used in SSDs.

TLC will also be one of the driving forces behind average capacity increase. The main obstacle in SSD adoption is obviously the cost per gigabyte, and the lower production costs of TLC will help to bring the prices down. I think it's too early to say what kind of impact TLC will have on prices because currently there are only two drives available (SanDisk's Ultra II and Samsung's 840 EVO), but once more OEMs are ready with their TLC SSDs later this year and early next year, I believe we will see more aggressive pricing.

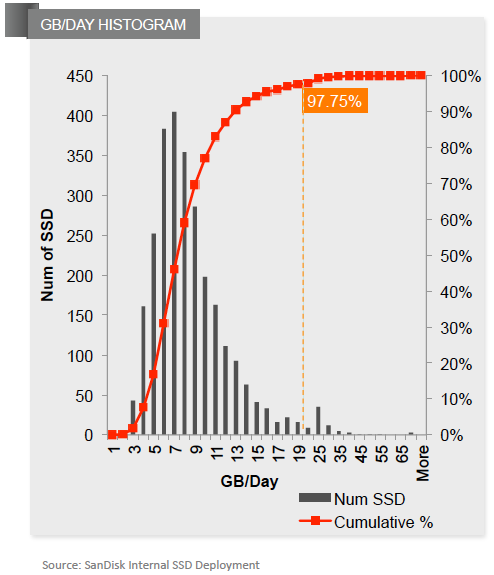

One of SanDisk's presentations at the show had a very interesting slide about the company's internal SSD deployment program. The question that is often debated when it comes to SSD endurance is the number of gigabytes that a user writes per day. There aren't really any studies with large sample sizes, but SanDisk's own study provides an interesting insight into typical office workloads.

What the data shows is that a typical office user only writes about 7GB per day on average and the number of people that write over 20GB is only a few percent, so very few users actually need more endurance than what TLC SSDs can offer (~20GB/day). Of course, everyone's usage is different and I doubt SanDisk's data takes e.g. media professionals properly into account, but it is still interesting and valuable data nonetheless.

Another thing I discussed with SanDisk was the obstacles for higher SSD adoption rate. While there is growth, the attach rate in the consumer space is still fairly modest and will remain as such for the next few years at least. Price is obviously one of the most important factors as hard drives are still an order of magnitude cheaper when measured in price per gigabyte, but I'm not sure if absolute price and capacity are the only hurdles anymore. I mean, 256GB is more than sufficient for the majority of users – especially now that we live in the era of Netflix and Spotify – and at ~$100 it's fairly affordable, so I think we have reached a point where the price is no longer the barrier preventing users from upgrading to SSDs.

This is actually the part where we ask for your, our readers, help. What is it that we or manufacturers like SanDisk could do to boost the SSD penetration in the market? Would live demonstrations at malls and other public places help? Or upgrade programs where you could take your PC to a store and they would do the upgrade there for you? Let us know your ideas in the comment section below and I'll make sure to bring them up with SanDisk and other SSD manufacturers. Remember that we are talking about the masses here, so think about your parents for instance – what would it take for them or other people who are not very comfortable around computers to upgrade their PCs with an SSD?

The one huge problem is of course the PC OEMs and convincing them to adopt SSDs for mainstream laptops. The race to the bottom practically killed the profits in the PC industry, which is why most of the mainstream (~$400-600) laptops have such a bad user experience (low-res TN panels, cheap plastic chassis, etc...). With already razor thin margins, the OEMs are very hesitant about increasing the BOMs and taking the risk of cutting their already-near-zero margins with SSDs. I know SanDisk and other SSD OEMs have tried to lobby SSDs to the PC OEMs as much as possible, but anything that adds cost gets a highly negative response from the PC OEMs.

The Enterprise

In mid-July SanDisk announced their acquisition of Fusion-io and the acquisition was completed a couple of week prior to Flash Memory Summit. I posted my initial thoughts when the news hit the public, but I feel that it's worth doing a bit deeper analysis now that I have given it some more thought and discussed it with John Scaramuzzo, senior vice president and general manager of SanDisk's enterprise business.

SanDisk has managed to establish itself as one of the key players in the enterprise SSD space over the past few years. The acquisitions of Pliant in 2011 and SMART Storage Systems in 2013 provided SanDisk with strong expertise and product lineups for SATA and SAS SSDs but left the company without a solid long-term plan for PCIe. I heard Pliant's initial roadmap included plans for PCIe-based solutions as well, but it looks like those plans never materialized.

Up until the Fusion-io acquisition, the Lightning PCIe SSA was the only PCIe solution in SanDisk's enterprise product portfolio, and as a matter of fact that drive is internally a SAS-based design with a PCIe to SAS bridge onboard. In other words, SanDisk had practically zero real PCIe solutions for the enterprise, while at the same time SanDisk's biggest competitors, such as Intel and Samsung, have had PCIe drives for a long while already.

Fusion-io's 3.2TB Atomic Series SSD

Fusion-io's strategy and product portfolio, on the other hand, was a complete opposite. From the beginning Fusion-io has focused on PCIe storage, which dates all the way back to 2007 when the company released its first ioDrive that utilized a PCIe x4 interface and was capable of speeds up to 800MB/s. Not only was Fusion-io early in the market, but the company was also able to garner a few massive and very important clients – the most notable being Facebook and Apple. I don't think it's an overstatement to say that Fusion-io can be considered as the pioneer of PCIe storage because it was the first company to turn PCIe SSDs and storage in general into a large, successful business.

But stories eventually come to an end. The competitive advantages Fusion-io had were its PCIe technology and several high-level customers, but the advantages were lost when the NAND manufacturers stepped into the PCIe territory. It's nearly impossible for a company that has to source its NAND from a third party to compete against another company that manufactures NAND in-house since the latter will always have advantages in cost. While Fusion-io didn't lose its customers to competitors overnight, it's clear that especially Intel and Samsung snagged a share of Fusion-io's business in the past couple of years.

In a nutshell, the acquisition brings SanDisk the long-needed expertise in PCIe storage along with Fusion-io's broad PCIe product portfolio. The acquisition is now a bit over 100 days in and the Fusion-io employees have been integrated into SanDisk's existing teams. Initially Fusion-io's engineering team was separate and worked under Lance Smith, the former President and COO of Fusion-io, but Mr. Smith decided to leave SanDisk and pursue other options. Last week a data virtualization startup Primary Data announced that Mr. Smith has joined the company as the new CEO, which explains his quick departure from SanDisk.

All the engineering talent has now been unified and the team is lead by Mr. Scaramuzzo. With everyone under the same roof, the roadmaps are now in the process of being integrated to bring the expertise together. It will be a while before we see the fruits of the acquisition, but in the meantime the latest Fusion-io products will transition to SanDisk NAND for increased cost efficiency.

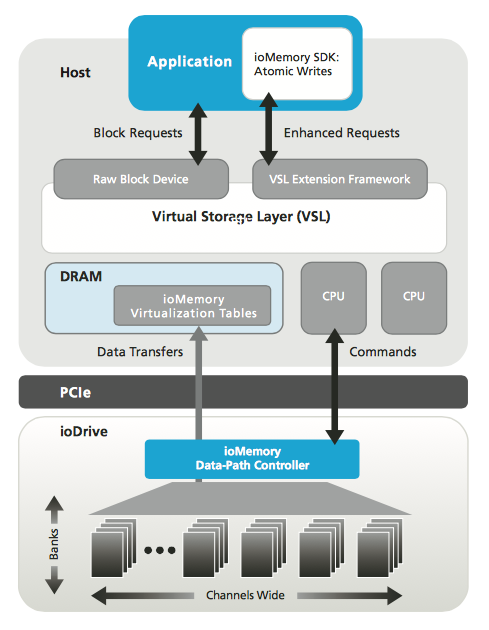

But what about NVMe? That has been the hot topic in the industry this year and I bet many of you are wondering what is SanDisk's and Fusion-io's play in that field. The short version of their strategy is that Fusion-io already has a technology called Virtual Storage Layers (VSL), which is essentially a driver/software stack similar to NVMe. The truth is that NVMe isn't really anything new from a technology perspective, but what makes it alluring for many manufacturers is the fact that the NVMe drivers are universal and already supported by the latest operating systems. Technologies like VSL are rather expensive to develop and require expertise because there is no framework available (i.e. everything has to be developed from scratch), but on the other hand an in-house driver like VSL allows for more customization and optimization.

However, that doesn't mean that SanDisk has no interest on NVMe whatsoever. The company sees that as the entry and mid-level enterprise SSDs move from SATA and SAS to PCIe, NVMe will be one of the key factors because of easy and quick deployment. For that market segment the NVMe spec and its limitations are fine – it's only the high-end segment where the benefits of VSL are more prominent. It's actually likely that many manufacturers will turn to custom NVMe drivers anyway for higher and more optimized performance, and in fact that is already happening with Intel providing its own NVMe driver for the P3600/P3700.

Lastly, let's quickly discuss the ULLtraDIMM. I wrote a quick piece on ULLtraDIMM right after Flash Memory Summit, but SanDisk has already scored Huawei as the third ULLtraDIMM partner (in addition to IBM and Supermicro). The first generation product that is currently available is internally based on a pair of SATA 6Gbps controllers, but SanDisk said that a native DDR to NAND controller is possible in the future if the market adopts the new form factor well. As usual, the industry is fairly slow in adopting new form factors, so it's hard to say whether NAND DIMMs will really take off, but it's a very interesting and potentially useful technology.

Final Words

All in all, SanDisk is definitely one of the most interesting NAND companies going forward. USB drives, eMMC solutions, SSDs and even the storage arrays from the Fusion-io acquisition are all built on NAND, which puts SanDisk in a unique position as it's the only NAND manufacturer that focuses solely on NAND products. The company can't turn to alternative revenue sources like e.g. Intel and Samsung can, but on the other hand that's also SanDisk's strength as all the know-how and experience in the company is related to NAND in one way or the other.

Ultimately next year will be crucial for SanDisk because it determines whether the company can materialize all the underlying potential from the Fusion-io acquisition and become a serious competitor to Intel and Samsung in the enterprise space. The pieces are definitely there, so it's just a matter of execution now.