Original Link: https://www.anandtech.com/show/10315/market-views-hdd-shipments-down-q1-2016

Market Views: HDD Shipments Down 20% in Q1 2016, Hit Multi-Year Low

by Anton Shilov on May 12, 2016 8:00 AM EST

Leading industry watchers like IDC and Gartner early this year predicted that the first quarter of 2016 would not be good for the PC industry and various companies agreed with that. The reasons for the declines are well known: global economic issues, the slowdown in China, the strong U.S. dollar as well as competition from smartphones and other devices. As sales of PCs were not strong as predicted, this negatively affected the hard drive market.

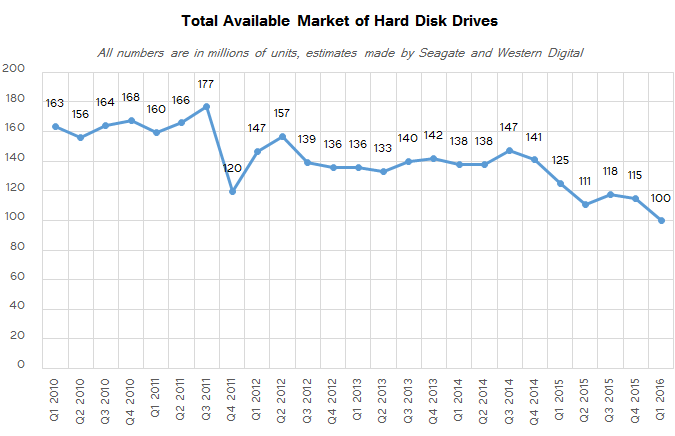

According to Gartner, PC shipments worldwide totaled 64.8 million units in the first quarter of 2016, a decrease of 9.6% from Q1 2015. The company notes that this was the first time since 2007 that shipment volume fell below 65 million units. Analysts from IDC are even more pessimistic because based on their findings, shipments of PCs in the first quarter totaled 60.6 million units, a year-over-year (YoY) drop of 11.5%. As we noted in our previous coverage of the HDD market earlier this year, the decline of HDD shipments in 2015 significantly outpaced the regress of the PC market. As it appears, the same happened in the first quarter of 2016 as the total available market of hard drives dropped to a new multi-year low.

Shipments of HDDs Total 99.8 Million Units in Q1 2016

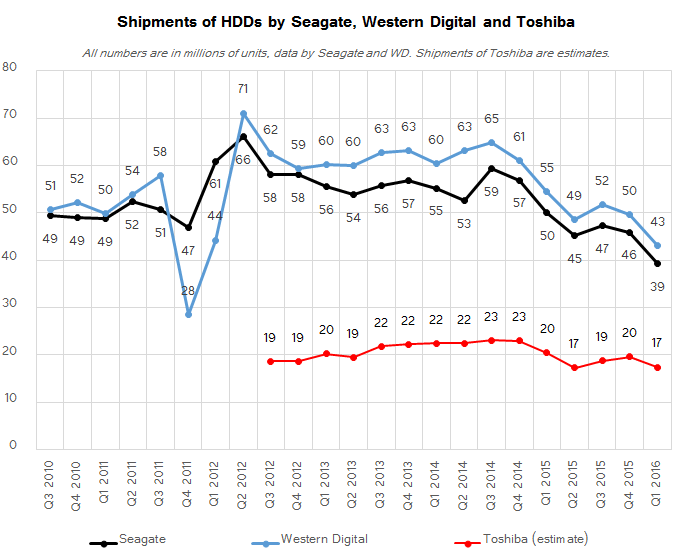

Seagate, Toshiba and Western Digital, the three remaining producers of HDDs, shipped a total of 99.8 million hard drives in Q1 2016, or 20% less than in the same period a year ago according to their estimates (see counting methodology below). According to estimates from Nidec, the company that sells the majority of small precision motors for HDDs (over 80% of them, based on its own estimates), the industry sold 98 million hard drives in Q1, but it is worth noting that Nidec is typically very conservative. In the same quarter of last year, Seagate, Toshiba and Western Digital sold 125 million HDDs, whereas just six years ago the industry shipped 163 million units. In fact, even in Q1 2006, sales of HDDs totaled 101.7 million units, according to iSuppli (via EDN), which means that we might be talking about a 10-year low in hard drives shipments.

Sales of PCs in general (and hard drives in particular) are seasonally not strong in the first quarter of the year, which is why it is not surprising that they declined to around 100 million units from 115 million units in Q4 2015. What is alarming is that despite this seasonal change, Q1 2015 shipments of HDDs were higher than sales of hard drives in each of the remaining quarters last year. If this year follows the same negative pattern, then HDD shipments will be below 100 million units in the second quarter and will remain below that level in the second half of the year. Western Digital estimates that total available market (TAM) of HDDs will decline to 95 million units in the second quarter, which means a decline of around 15% from the same period last year. A moderately good news is that Western Digital seems to be optimistic about the second half and believes that HDD TAM will remain above 400 million units mark in 2016 (compared to 456 million units in 2015), which means that shipments of hard drives will grow in calendar Q3 and calendar Q4. IDC has asserted that inventory reductions, cautious buying and other additional elements of the equation that directly affected makers of components in the recent quarters are wrapping up, Western Digital’s optimism could well be justified.

Western Digital Remains World’s No. 1 HDD Supplier

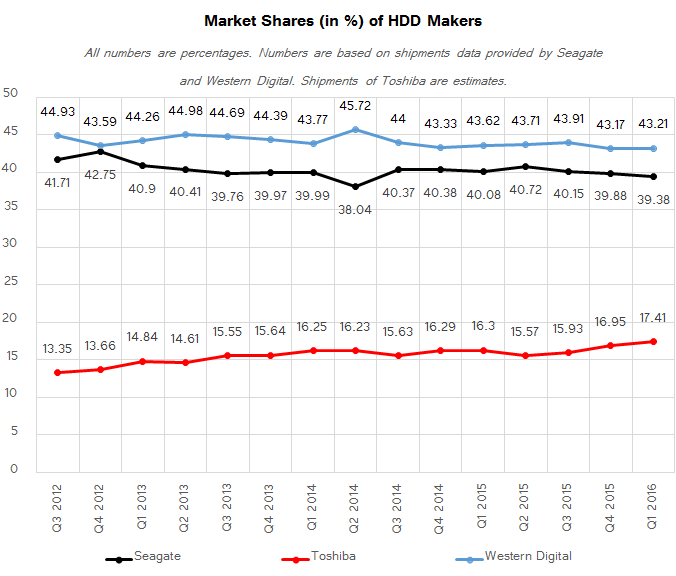

Due to severe declines in demand for hard drives, it does not look like HDD makers want to fight for market share. Western Digital controlled about 43% of the HDD market in Q1 2016, just like a quarter before. Seagate was the second largest supplier with 39.38% market share. If the HDD shipments numbers for Toshiba are correct, then the company controlled around 17% of the hard drive market, moving ever so slightly higher.

Seagate’s HDD Sales Drop Below 40 Million Units, Company Plans Capacity Adjustments, Product Cuts

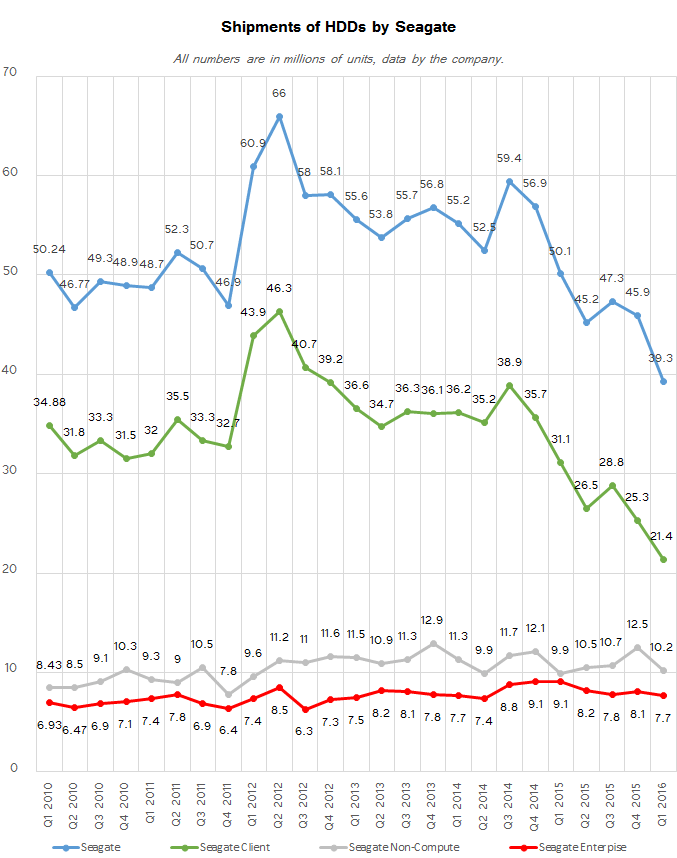

Seagate sold 39.3 million hard drives in the first quarter of 2016, a 21.5% decline from the same period a year ago. Sales of Seagate’s HDDs dropped across the board - with the exception of nearline drives. During the conference call with investors and financial analysts, the company particularly noted weak sales of client HDDs as well as declines in shipments of traditional mission-critical drives. Moreover, in a bid to maintain margins, the firm decided to “not aggressively participate in certain areas of the low capacity notebook market,” which further drove its unit sales down.

As it appears, Seagate does not seem to be confident that the hard drive market will rebound in the foreseeable future. The HDD maker intends to cut-down its manufacturing capacities from 55 – 60 million units per quarter to approximately 35 – 40 million units per quarter, which will help it to reduce operating costs and maintain prices despite competition from traditional and emerging rivals.

“In the March quarter we began the process of reducing our HDD manufacturing capacity from approximately 55 million to 60 million drives per quarter to approximately 35 million to 40 million drives per quarter,” said Steve Luczo, chief executive officer of Seagate, in a conference call with investors and financial analysts. “The actions required will be completed within the next 6 to 9 months. At the same time, we will continue to accelerate the utilization of our own drive factories internally and media facilities.”

While Seagate does not detail its capacity-cutting plans, it indicates that it intends to shift build volumes to its higher capacity models, which will simplify wafer requirements, optimize the lineup and will eventually reduce costs. In particular, the company will discontinue some of its low-capacity client HDDs (250 GB, 320 GB and 500 GB), which will help to increase its ASPs (average selling prices) and margins.

“In [Q1 2016] we began end-of-life activity on some of the older 500 GB and below products that have very low margins,” said Dave Mosley, president of operations and technology at Seagate. “Most of the margin cost benefits of these products will be realized over the next few quarters.”

In fact, Seagate began targeted pricing increases across its product portfolio already in the third quarter of its fiscal year (i.e., Q1 2016), which could help to improve its financial results. The manufacturer believes that higher HDD prices are justified because HDDs are getting harder to make. Since the company decided not to participate in some areas of the low capacity laptop market, it is evident that it may leave it to makers of entry-level SSDs in the future.

“In the March quarter we initiated targeted pricing increases across our product line, we were successful in some areas and unsuccessful in other,” said Mr. Luczo. “We continue to believe the industry needs a stable pricing environment to deliver the higher level of requirements being placed on our products and to realize the value we are providing to the market. As a result, we will continue to pursue a pricing strategy that reduces and properly reflects the investment in technology the market requires.”

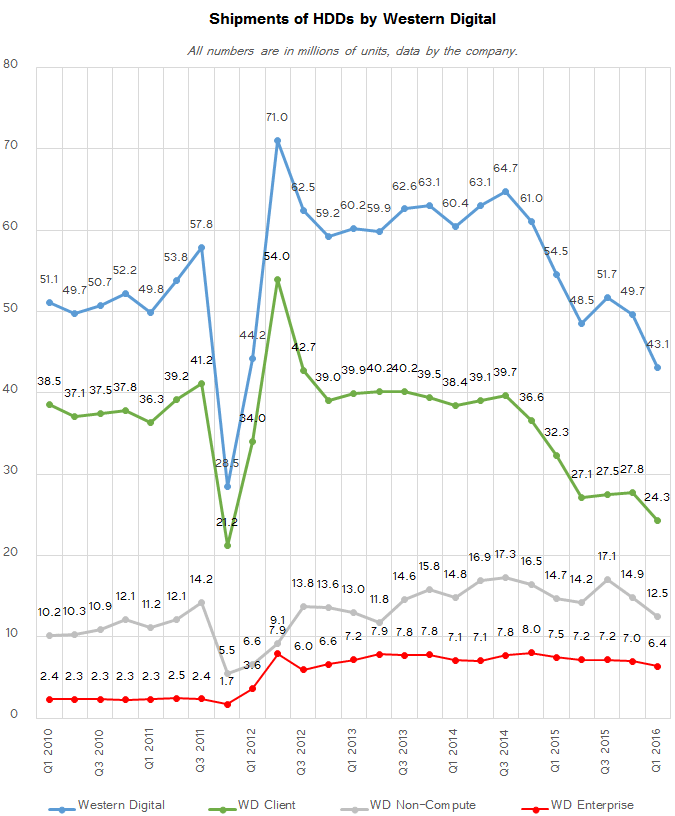

Shipments of Western Digital’s HDDs Fall to 43.1 Million Units

Western Digital shipped 43.123 million of HDDs in the first three months of this year, or 21% less compared to Q1 2015. Sales of the company dropped across the board due to the weak PC market and seasonality. Just like Seagate, Western Digital increased prices of certain products during the quarter. In particular, the company hiked prices of some of its 2.5” drives for notebooks and gaming PCs (which is probably the WD Black2 Dual Drive). Right now, the company is making selective price increases in the enterprise segment in a bid to maintain its ASPs and margins and sustain its ability to invest in the development of products.

“Because we want to make sure that we have got sufficient dollars to reinvest back into our business to continue to innovate and provide compelling products for our customers, we are making selective price increases in certain enterprise markets,” said Stephen Milligan, chief executive officer of Western Digital, in a conference call with investors and financial analysts. “At this point, we are not sure if they're going to stick, but we are certainly hoping that they do.”

Earlier this year Western Digital announced plans to optimize its roadmap and close-down its head wafer manufacturing facility in Otawara, Japan, in a bid to reduce costs and maintain its profitability. So far, the company has not announced plans to reduce its HDD manufacturing capacities significantly but said it would eliminate redundant facilities. The company also did not make any comments regarding the future of its low-end HDDs.

Toshiba’s HDD Shipments Drop Too

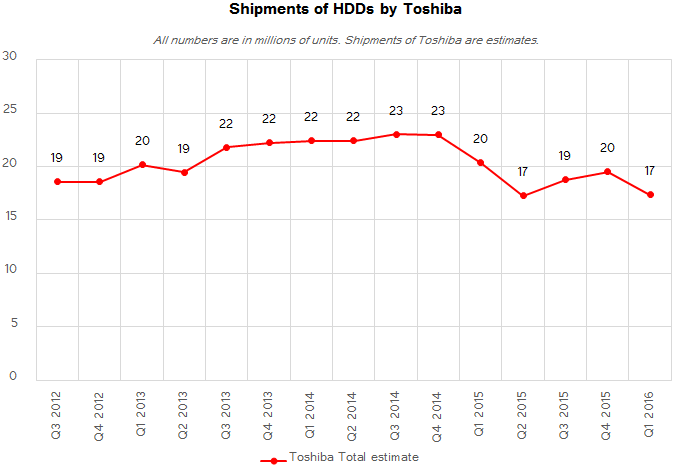

Since Toshiba does not disclose anything related to its hard drive business, it is hard to analyze this supplier. If estimations of HDD makers and Nidec are correct, then Toshiba’s HDD shipments in Q1 2016 should be around 17 million units, or 15% below its shipments in the same period last year.

Average HDD Capacities Continue to Increase

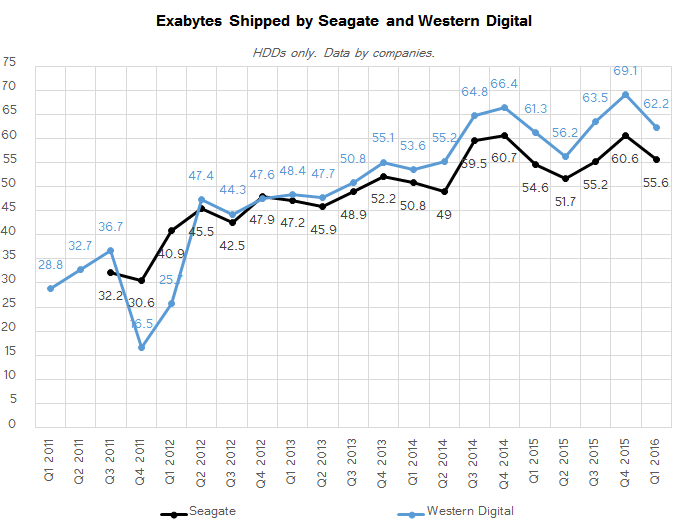

Despite the drop in HDD unit shipments, both sequentially and year-over-year, total capacities shipped by the two leading makers of hard drives increased in Q1. Seagate supplied 55.6 EB (Exabyte) of HDD storage last quarter, up from 54.6 EB in Q1 2015, but down from 60.6 EB in the previous quarter. The total capacity of Western Digital’s HDDs shipped in the first quarter of 2016 was approximately 62.2 EB, a moderate increase from 61.3 EB in Q1 2015.

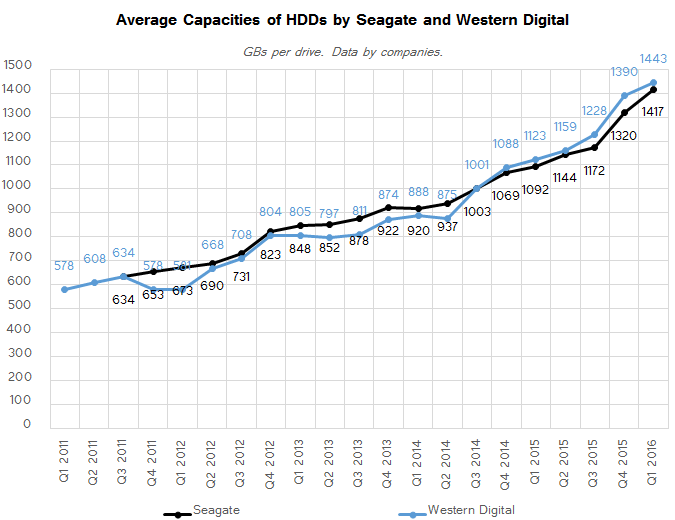

When it comes to hard drives, one thing that has been growing quarter-over-quarter for a long time now is average HDD capacity, particularly in the enterprise segment, but not only there. In Q1 2016, an average drive could store around 1.4 TB of data, an increase of 28.5% (Western Digital) and 29.7% (Seagate) from the same quarter last year.

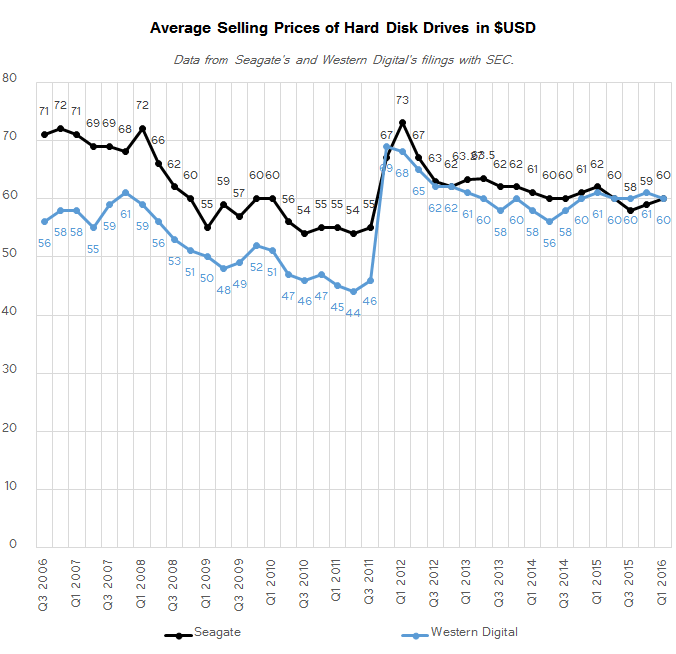

Average HDD Price Stays at $60 compared to Q1 2015

Despite the local price hikes by HDD makers, the industry can clearly produce more hard drives than it can consume, which is why prices of mass HDD models remain rather low. This will likely change in the future, when consumers shift to higher-capacity drives because of 4K UHD video or other reasons, but right now an average HDD from either Seagate of Western Digital costs approximately $60.

This will likely change after Seagate implements its plans to cut down its manufacturing capacities and supply-demand balance of the market will stabilize. However, it remains to be seen how significantly that is going to change going forward.

Shipments of Client HDDs as a function of all Client Drives Drop

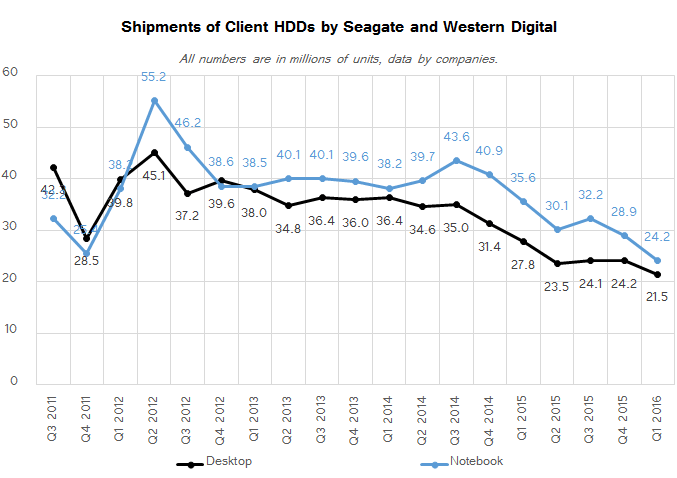

Long gone are the days when shipments of client HDDs by Seagate and Western Digital were around 75 million units per quarter. When PC sales drop to 60 – 66 million of units per quarter, it is simply impossible to sell that many drives. The two leading makers of HDDs supplied 45.7 million of hard disks in Q1 2016, down from 63.4 million from the same quarter last year. While Toshiba’s consumer drives should not be forgotten, it is evident that the increasing amount of new PCs use SSDs these days.

The SSD adoption rate in the notebook market in Q4 2015 was approximately 25~26%, according to TrendForce. In the first quarter that figure could easily go up because Seagate admitted that it did not want to play a part in certain areas of the low capacity notebook market. Moreover, as HDD platforms get more expensive in the coming years, hard drive makers may simply leave low-end bulk storage to SSD makers. In the end, it is relatively easy to build SSDs these days (it is not easy to manufacture NAND flash, of course), but HDD production involves a lot of R&D and state-of-the-art manufacturing facilities. As a result, companies like Seagate or Western Digital may simply lose interest in entry-level hard drives, especially given the fact that soon Western Digital will become a supplier of consumer SSDs as well.

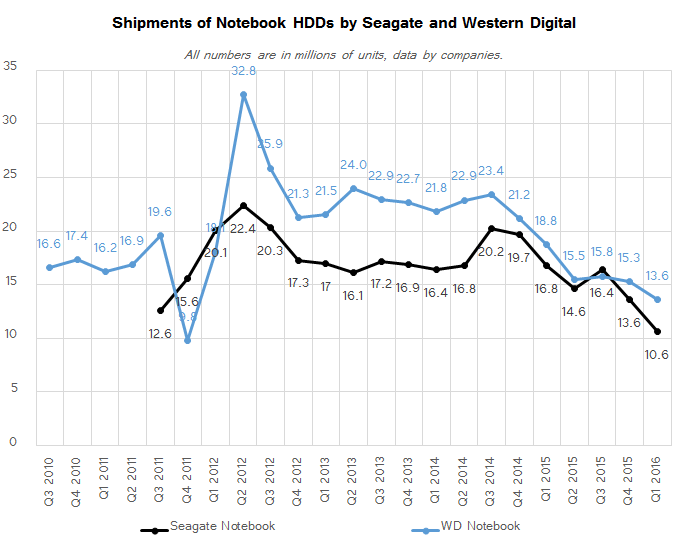

As pointed out in the previous report, Seagate includes shipments of hard disk drives it sells for game consoles into its 2.5” client HDD category, whereas Western Digital includes its drives for consoles into its consumer electronics category. As a result, the picture is somewhat noisy here. Seagate sold 10.6 million 2.5” client HDDs in the first quarter, which is a drop of 37% from the same period a year ago. Since the company deliberately decided not to fight for low-end notebook deals, such a sharp decline is not something unexpected. Meanwhile, Western Digital supplied 13.6 million of its 2.5” client hard drives in Q1 2016, 28% less than in the same quarter last year.

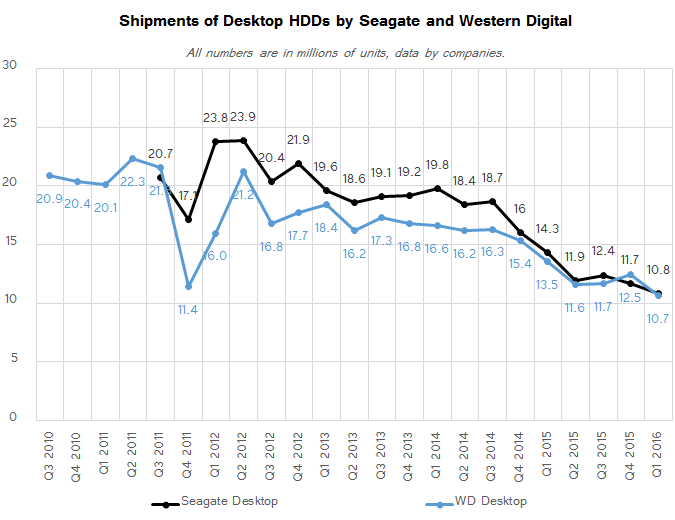

Sales of client 3.5” HDDs by Seagate and Western Digital declined by 22.8% year-over-year, in line with the deterioration in the HDD market. Moreover, actual shipments of desktop hard disks were on the same level for the two leading makers: Seagate supplied 10.8 million units (a 24.5% drop YoY), whereas Western Digital shipped 10.7 million devices (a decrease of 21% YoY). We do not know how many 3.5” client hard drives Toshiba shipped in Q1, but it is safe to say that the market is on the decline in general and it does not make a lot of sense to fight for desktop market share these days.

In its recent conference call with investors and financial analysts, Seagate re-emphasized that it expected sales of its client drives to continue declining, but to keep gaining capacity. Historically, sales of Seagate’s client HDDs accounted for 60% of its revenue, whereas sales of enterprise products accounted for 40% of its revenue. Given the current market trends away from installing HDDs into tablets, 2-in-1 hybrid PCs or ultra-thin notebooks, client HDD revenue will eventually drop to 40% of Seagate’s revenue whereas enterprise hard drives will account for 60% of its revenue, the company revealed. With that said, it is expected that Seagate will focus on higher-capacity drives rather than on inexpensive devices that help to boost unit sales, as the latter is not something that is needed ion a weakening market.

Sales of External HDDs and NAS Fall

Because the number of PCs that cannot house more than one internal storage device is growing, external storage is getting some traction. Seagate and Western digital offer broad lineups of DAS and NAS devices under their own trademarks as well as under G-Technology and LaCie brands. While shipments of branded storage products do not drive huge volumes, this is a rather lucrative business for manufacturers offering higher ASPs.

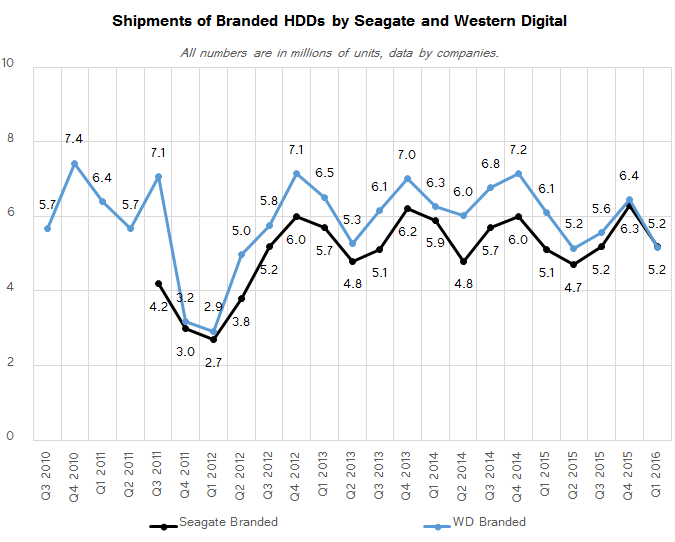

Sales of branded DAS and NAS devices by Seagate and Western Digital totaled 10.357 million units in the first quarter of 2016, down 7.5% from 11.190 million units in Q1 2015. The two manufacturers sold an equal amount of external storage products: Seagate shipped 5.200 million branded devices (up 2% YoY), whereas Western Digital sold 5.157 million branded products (down 15.3% YoY). Historically, Western Digital outsold its main competitor with its My Cloud and My Passport external HDDs, but in the recent quarters Seagate has begun to catch up whereas sales of WD began to decline.

One thing that should be kept in mind when analyzing branded storage is that no matter how many HDDs are inside a DAS or a NAS, they are all considered as one unit (e.g., a WD My Book, a WD My Book Duo and a fully-populated My Cloud DL4100 are equal from accounting perspective). As a result, while we do see that unit sales of branded external storage by the two large makers have been slowly declining in the recent quarters, we do not know anything about the exact amount of drives inside as well as their storage capacities.

Consumer Electronics Still Consume A Lot of HDDs

The vast majority of consumer electronics (CE) devices nowadays use NAND flash memory. However, applications like set-top-boxes, DVRs, surveillance systems and game consoles remain sizeable consumers of hard drives, which is why makers of HDDs develop platforms specifically tailored for such devices.

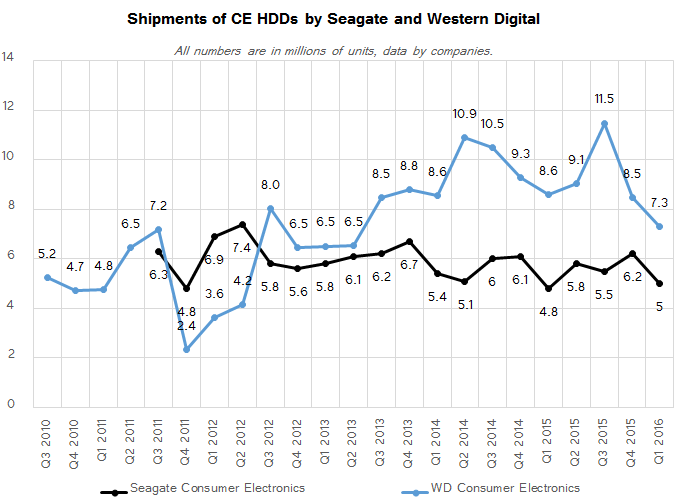

Since shipments of Seagate’s CE HDDs do not include drives it supplies for game consoles (they are included in client 2.5” HDD sales), its CE business looks relatively stable and mostly driven by seasonality. In the first quarter of 2016, Seagate sold 5 million of CE HDDs, slightly up from 4.8 million supplied in the same period a year ago.

By contrast, Western Digital recognizes HGST Travelstar HDDs for Sony’s PlayStation 4 as consumer drives, which is why its CE numbers significantly depend on the production of PS4. Since in Q1 console sales and manufacturing are not on the rise, sales of Western Digital’s CE HDDs declined to 7.3 million units, down 15.2% from Q1 2015. The reasons for the drop are unclear - perhaps Sony decided to slow down PS4 production, or perhaps shipments of some other Western Digital products were not strong.

Anyway, due to account policies of the two leading makers of hard drives, it is impossible to compare their CE HDD businesses directly.

Unit Sales of Enterprise HDDs Decline, But There Is a Catch

Enterprise hard disk drives are arguably the most important and lucrative part of HDD makers’ business these days. Firstly, such drives have to use many leading-edge technologies in order to demonstrate very high performance, or offer very high capacities. Secondly, they are not shipped in huge volumes, but they are sold with huge premium because of the technologies as well as extended reliability. Finally, since many client devices no longer have HDDs, but still have to store files elsewhere, their data ends up in the cloud and stored on various datacenter-class HDDs. Basically, even if an HDD maker fails to sell a $50 drive for a low-end laptop, the data from that laptop will eventually be stored on a $300 - $600 nearline drive in a data center, compensating missed revenue to the HDD producer.

There are two types of enterprise-class hard drives:

- High-performance HDDs for mission-critical storage that feature 10K or 15K spindle speeds as well as SAS interface. Such drives compete against SSDs these days and their volumes are slowly declining. This trend has been ongoing for years now and hard drive makers perfectly understand it. Seagate, Toshiba and Western Digital also offer high-end mission critical SSDs with SAS interface to their customers and eventually the portfolio of such solid-state storage devices will only expand.

- Another type of enterprise HDDs are nearline (near online) drives that are used to store various data in data centers. Some of such drives are for cold archives, which are rarely accessed and are hardly ever modified. Such HDDs have 5400 RPM-class spindle speed and their main purpose is to store as much data as possible and at the lowest cost. Other drives are used to store frequently accessed and modified data, which is why they feature 7200 RPM spindle speed and various methods to improve their performance. These drives can be filled with helium to maximize storage space (allowing a reduced platter gap) and keep power consumption down to minimize TCO. Usage of nearline HDDs has been increasing in the recent years. More importantly, their capacities have been growing very rapidly.

It is very important to distinguish between the two types of enterprise-class hard drives not only because they are completely different from a technology point of view, but also because their market dynamics are poles apart. Unfortunately, until this quarter neither of HDD makers disclosed sales of mission critical and nearline drives separately, but only reported the number of enterprise-class HDDs sold. This quarter, Seagate published more or less precise details about its enterprise drives and their dynamics, which we will analyze below. In the meantime, let’s have a look at the shipments of both leading enterprise HDD suppliers.

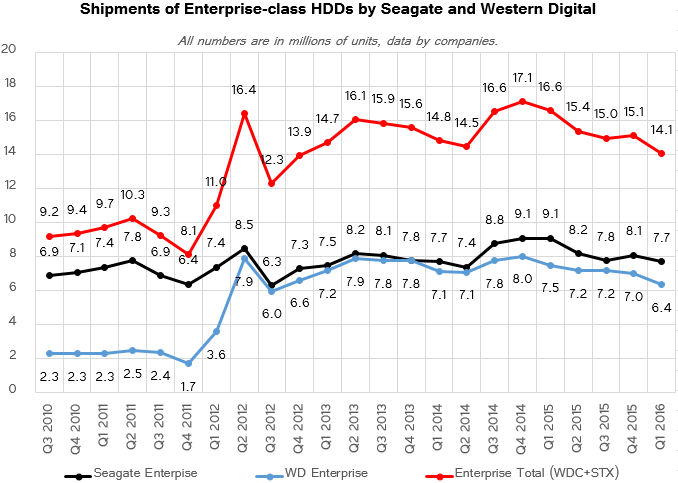

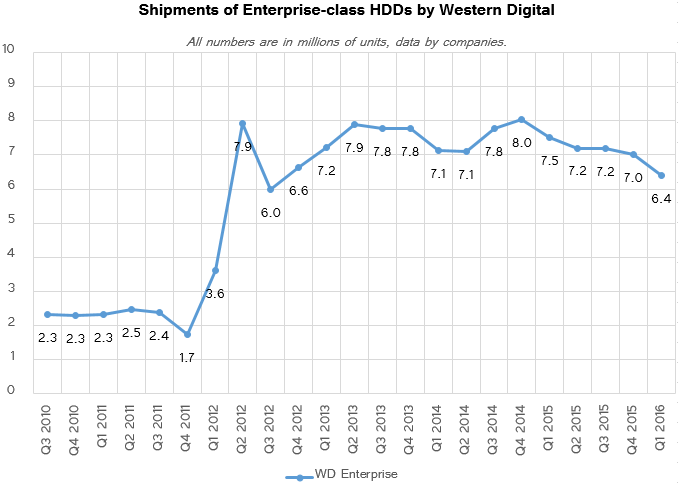

Based on the numbers from Seagate and Western Digital, sales of enterprise-class hard drives from these two manufacturers declined to 14.09 million units in Q1 2016, which is 15% lower compared to the first quarter last year. Seagate remained the largest supplier of enterprise drives with 7.7 million units sold (down 15.4% YoY), whereas Western Digital supplied 6.39 million of enterprise hard disks (down 15% YoY). Toshiba also has a portfolio of high-end drives for servers, but while it has many products with a SAS interface, it does not participate in the high-end of the nearline market due to lack of 8 TB and 10 TB HDDs in its lineup.

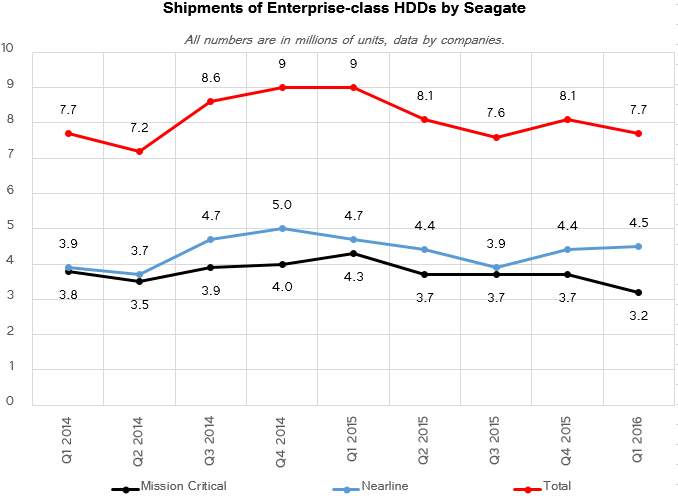

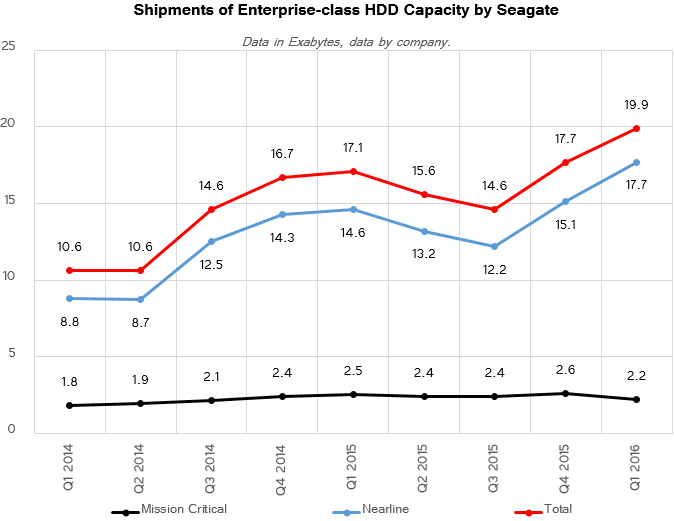

Out of 7.7 million enterprise drives that Seagate shipped in the first quarter, 4.5 million HDDs were for nearline storage applications, whereas 3.2 million HDDs were designed for mission-critical apps.

Shipments of Seagate’s nearline HDDs were down 4.3% compared to the first quarter of 2015, but were slightly up sequentially. The company claims that it expected demand for such drives to be significantly weaker, which is why it could not even satisfy all the demand. During the quarter, Seagate ramped up production of its 8 TB HDD lineup and significantly increased shipments of such drives compared to the previous quarter, however, it could not meet all the demand. The company also supplied a large volume of qualification units of its 10 TB helium-filled hard drives aimed at the highest-end of the cloud market. Due to the 7200 RPM spindle speed and advanced caching sub-system, Seagate’s Enterprise Capacity 3.5 (Helium) 10 TB hard drive is among the fastest in the company’s lineup, challenging even 15K mission-critical drives when it comes to sustained transfer rates (of course, those small drives still have a lot of other advantages, including considerably higher IOPS, significantly lower latency, very high instantaneous transfer rates and so on). In April, the company started revenue shipments of its SATA 10 TB HDDs, which further indicates growing demand for such drives.

By contrast, shipments of mission-critical HDDs dropped 13.6% sequentially and 25.6% year-over-year. The company says that approximately 25% out of 3.2 million mission-critical HDDs are 15K drives, which are gradually replaced by SSDs in the data centers. Solid-state storage devices also challenge 10K HDDs, but the manufacturer expects this segment of the market to have a much longer transition horizon. Because of the economic situation and the market shift to SSDs, sales of mission-critical drives were 700K below Seagate’s original forecast in Q1 2016, the company said.

Given the fact that nearline drives have significantly higher capacities than mission critical drives, it is not surprising that they are driving enterprise storage capacities in terms of EB shipments.

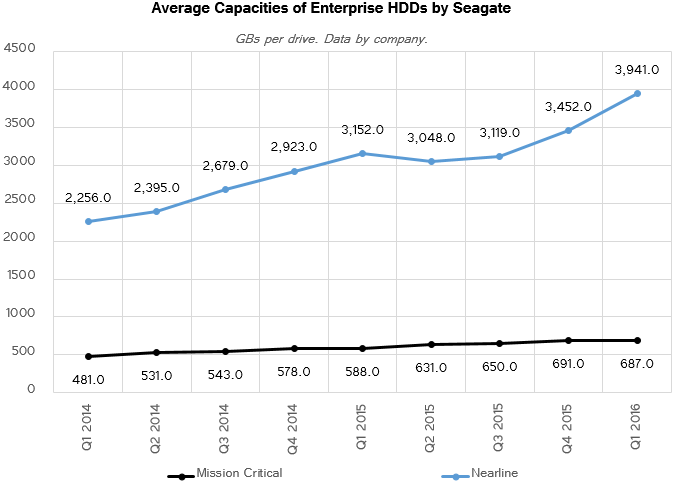

Average enterprise HDD sold by Seagate in Q1 2016 could store 3.941 GB of data, up 25% from the first quarter of last year, which is a direct result of growing demand for capacities from various data center customers.

Western Digital does not break down sales of its enterprise HDDs into nearline and mission critical categories, but while the split may be slightly different, market trends affect both companies in the same way. In its conference call with financial analysts, the management of Western Digital confirmed that shipments of the company’s 15K HDDs are declining because many customers replace such HDDs with SSDs and also observed that many 10K HDD deployments begin to adopt SSDs. In addition, the company noted that in Q1 2016 it saw steeper than expected price declines in performance enterprise and capacity enterprise markets. In particular, the company blamed decreased prices of 4 TB and 8 TB nearline HDDs for its lowering gross margins.

Final Words

The storage market in the first quarter of 2016 performed in accordance with the PC market trends in general. Shipments of HDDs went down, but sales of high-capacity nearline hard drives remained a bright spot in the reports of leading hard drive suppliers. Western Digital remains optimistic in the short term for HDDs, but Seagate detailed plans to severely cut its production capacities and to reduce its presence the market of low-end mobile HDDs.

As ultra-thin notebooks, as well as 2-in-1 hybrid PCs, are gaining market share, the potential for 2.5” client HDDs suffers. Theoretically, sales of 2.5” drives for AIO and small form-factor desktops could offset declines in the mobile (at the expense of 3.5” HDDs declines), but this did not happen in Q1: sales of Seagate’s 2.5” client HDDs dropped to 10.6 million units (down 37% YoY), whereas shipments of Western Digital’s 2.5” client drives declined to 13.577 million units (down 28% YoY).

This quarter Seagate announced plans to discontinue some of its 2.5” low-capacity (500 GB and lower) client drives and concentrate on promoting 1 TB and 2 TB 2.5” models based on its latest technologies. Basically, Seagate no longer wants to compete against entry-level TLC NAND-based SSDs in low-end and mainstream notebooks. Reducing participation in this market segment will allow Seagate to simplify the portfolio of components it purchases from other makers and cut down its costs as high-capacity platters for advanced drives are made mostly in-house. It will be very interesting to see how other HDD makers respond to this action. They face similar problems and eventually it will only get harder to compete against cheap SSDs.

Shipments of 3.5” client hard drives hit a new low in the first three months of this year, which was not completely surprising, given slow shipments of PCs. So far neither Seagate nor Western Digital has announced plans to optimize their 3.5” lineups (WD actually folded its Green drives into its Blue lineup last year), but this is something that will likely happen in the future.

Enterprise HDD business is a mixed bag these days. On the one hand, sales of 10K and 15K HDDs are declining because of SSDs and that decline has yet to bottom out. Yet, those hard disks remain expensive and the business overall is profitable. On the other hand, sales of nearline drives are on the rise. More importantly, the growth of average capacities of such HDDs even outpaces the growth in their unit sales. Interestingly, Seagate indicated that demand for high-end 8 TB nearline HDDs was so strong in Q1 2015 that it could not even fulfill the orders placed. Seagate’s rather unexpected start of 10 TB HDD revenue shipments in April proves that operators of data center are rapidly building up capacities.

Seeing the fact that HDD sales volumes have been falling for many quarters now, Seagate not only decided to exit the market of low-end notebook drives but also detailed its plans to steeply cut-down its manufacturing capacities to 35 – 40 million units per quarter from 55 – 60 million units per quarter. From now on, the company will focus on high-capacity HDDs that are sold at higher prices rather than on affordable drives for bulk storage, which will naturally help it to avoid direct competition against SSDs in the entry-level segment where capacity may not be that important. It remains to be seen what Seagate will do with the manufacturing equipment that it will not need after its optimizations, but that is a different conversation entirely.

Looking ahead, Western Digital believes that the HDD TAM will remain above a psychologically important 400 million units per year mark (shipments of HDDs last year were around 453.6 million units), but will drop in the long term. Meanwhile, Nidec conservatively predicts that HDD TAM will fall to 400 million units in 2016 with shipments of PC and external HDDs declining the most. The upcoming quarters will show whether optimistic or conservative predictions are applicable to today’s HDD market.

Methodology and Important Notices

There are three major manufacturers of hard drives today: Seagate, Toshiba and Western Digital. Other suppliers are reselling hard drives made by these three companies.

Seagate and Western Digital reveal their HDD unit shipments as well as TAM (total available market) estimates every fiscal quarter. While such numbers are considered preliminary, they are usually rather accurate and re-affirmed by third-party analysts. Our TAM is the midpoint between Seagate’s and Western Digital’s TAM estimates. If only one hard drive maker reveals its TAM, we consider the number from only one vendor.

Meanwhile Toshiba does not officially disclose its HDD shipments. We subtract quarterly shipments of Seagate and Western Digital from our TAM estimate to get the number of drives sold by Toshiba. The approach is is the reason why we do not report historical shipments of Toshiba prior to Q3 2012. Based on estimates of hard drive makers and industry observers, Toshiba cannot produce more than 22 – 23 million of HDDs per quarter.

Seagate’s and Western Digital’s fiscal quarters end on the last business day of the last week of a calendar quarter (e.g., the Friday next to December 31). While fiscal quarters of HDD makers may not correspond exactly to calendar quarters, they are very close. Fiscal years of Seagate and Western Digital do not correspond to calendar years as they begin in July.

Historical TAM data comes from financial reports of Seagate and Western Digital.

Note 1: Seagate completed the acquisition of Samsung’s HDD business in December, 2011. The company started to include sales of Samsung-branded HDDs in its quarterly shipments in Q1 2012 (Q3 FY2012).

Note 2: Western Digital closed the acquisition of Hitachi Global Storage Technologies in March, 2012. Western Digital began to include HGST shipments in its financial reports in Q2 2012 (Q4 FY2012).

Note 3: Toshiba acquired some of Western Digital’s 3.5-inch HDD manufacturing equipment and intellectual property in May, 2012. It was expected that the manufacturing transfer could be complete within 6 to 12 months. Western Digital made HDDs for Toshiba on a contract basis until late Q4 2012. Due to the contract manufacturing agreement between Western Digital and Toshiba in 2012, there may be some inaccuracies in the historical data in that period (i.e., since the drives were made by Western Digital and then sold to Toshiba, they are attributed to the former, not the latter).

Note 4: Seagate defines client HDDs as 2.5” and 3.5” hard drives for desktops, notebooks and hybrid PCs as well as game consoles. Seagate considers HDDs for external storage and network-attached storage (NAS) as “branded” drives. Hard disks for DVRs and surveillance systems belong to Seagate’s family of HDDs for consumer electronics. Enterprise lineup includes 2.5” and 3.5” drives for mission critical (SAS, SCSI, Fibre Channel), enterprise storage, nearline and other datacenter applications.

Note 5: Western Digital attributes desktop and mobile 2.5” and 3.5” hard drives to client HDDs. External hard drives and NAS are referred to as “branded products”. Western Digital’s consumer electronics HDDs are used in DVRs, game consoles, video streaming applications and security video recording systems.